Your best hourly worker just quit. Not over pay. Over timing. They earned the money on Tuesday, the car broke down on Wednesday, and payday was still nine days out. A $300 gap turned into a payday loan, then a missed shift, then a resignation.

That gap is now a benefit category. Earned wage access software lets employees pull a portion of wages they have already earned before the scheduled payday, without changing your payroll cadence or fronting the cash yourself. The employer-sponsored segment is projected to grow from $5.9B in 2026 to $16.86B by 2030, a 30% CAGR, according to Research and Markets (2024). That growth is not hype. It tracks a real operational problem: financial stress drives turnover, and turnover is expensive.

For a founder or operator, the appeal is narrow and specific. This is a recruiting and retention lever you can roll out fast, integrate with your existing payroll, and defend on ROI without a six-figure line item. The friction shows up in the details: which provider charges what, who handles compliance exposure under state laws and federal lending rules, and whether the employee experience is clean enough that people actually use it.

If you are early in evaluating operational tooling, it helps to compare categories the way you would compare any stack decision. The same skepticism you apply when weighing ai recruiting software or ai customer service software applies here: stack fit, speed to value, and what it actually replaces. This guide ranks eight earned wage access providers and shows you which one fits which workforce.

What's inside

This guide covers eight earned wage access platforms and ranks them by relevance to employers comparing options in 2026. We selected tools based on four criteria that matter most for a fast, defensible rollout: fee transparency for both employer and employee, depth of payroll and HRIS integration, the quality of the employee app experience, and compliance posture. You will get a comparison table, a definition section for anyone new to the category, item-by-item breakdowns with verified pricing and G2 ratings, and a buyer's checklist. The goal is a decision, not a brochure. By the end you should know which provider fits a small business, which fits an hourly-heavy workforce, and which fits an enterprise already inside a payroll ecosystem.

TL;DR

- Best overall for broad functionality and payroll integration: Tapcheck, with no-code payroll and timekeeping integration and free employer cost.

- Best for low-fee, employee-friendly access: Payactiv, with no-fee ACH transfers and deep financial wellness tools.

- Best for brand recognition and engagement depth: DailyPay, a widely adopted on-demand pay platform.

- Best for consumer-style access with no mandatory fees: EarnIn, where standard Cash Out transfers are free.

- Best for workforce payments plus wallet features: Branch, combining payouts with a digital banking app and card.

- Best for SMB rollout: ZayZoon, free for employers to offer with a flat employee fee.

- Best for fee transparency: Chime Workplace, fee-free for employers and employees.

- Best for payroll-linked card workflows: Wisely® by ADP, for teams already inside the ADP ecosystem.

What is earned wage access software?

Earned wage access software is a payroll-linked platform that lets employees access a portion of the wages they have already earned before their scheduled payday. It sits between your timekeeping data, your payroll system, and an employee-facing app, calculating how much an employee has earned and making some share of it available on demand.

You will see the same idea sold under several names. On-demand pay, early wage access, instant pay, and earned wage access app all describe the same core mechanic: money the employee has already worked for, available before the normal pay cycle closes. Vendors mix and match these terms, so treat them as synonyms when you compare.

Here is how the category works in practice:

- What EWA means: Employees draw against wages already earned, not a loan against future pay. There is no interest and no traditional credit check on the access itself.

- How payroll, HRIS, and timekeeping integrations work: The platform connects to your payroll provider, HRIS, and timekeeping system to read hours worked and calculate available earnings. The cleaner the payroll integration, the less manual reconciliation lands on your team. Strong HRIS integration keeps employee eligibility and status accurate, and timekeeping integration drives the real-time available-balance number.

- What employees see in the app: A running balance of accessible earnings, transfer options (instant or standard), pay stub visibility, and often budgeting or savings features layered on top.

- Why compliance matters: Depending on the funding model and fee structure, a program may or may not trigger lending regulations. State laws differ, and federal frameworks like Regulation Z and the Truth in Lending Act (TILA) sit in the background. Provider structure determines your exposure.

- Why fees and transparency are buying criteria: Some programs are free to employees; others charge per-transfer or instant-transfer fees. Transparent, predictable fees protect both employee trust and your reputation as the employer offering the benefit.

The category overlaps with broader financial wellness thinking: the point is to reduce financial stress between paychecks without restructuring how you actually run payroll.

When to use earned wage access

Reduce turnover in hourly or shift-based workforces

Turnover is brutal in hospitality, retail, healthcare, and field services. Every open shift you cannot fill is lost revenue, and every replacement hire carries recruiting and ramp cost. Earned wage access gives hourly workers a buffer for the cash-flow gaps that push them toward a second job or a competitor offering the same wage plus on-demand pay. When two employers pay the same hourly rate, the one with instant pay access often wins the candidate. For employee retention in shift-based teams, this is one of the lowest-overhead levers available.

Improve financial wellness without changing payroll cadence

You do not have to move to daily payroll to support workers between paychecks. That is the operational elegance of the category. Your payroll keeps running on its normal cycle, your finance team keeps its existing process, and the EWA provider handles the funding and access layer in between. Employees get financial flexibility; you avoid the cash-flow and accounting disruption of accelerating your entire payroll calendar.

Add a benefit that is easy to explain and fast to deploy

For a founder evaluating any new tool, the test is first-win speed and stack fit. The strongest earned wage access platforms install through no-code payroll integration, require little ongoing admin, and explain themselves to employees in a sentence. That makes EWA easy to roll out, easy to communicate during recruiting, and easy to defend to a board because the cost to the company is often zero. The same evaluation discipline you would apply to ab testing tools or agentic ai platforms works here: does it earn its place in the stack inside the first quarter?

Comparison table

The table below ranks the eight earned wage access software options by relevance to employers in 2026. Use it to scan fee transparency, payroll integration strength, employee experience, and compliance posture in one place before reading the full breakdowns. Pricing and ratings reflect verified, current values from each vendor and G2.

| # | Product | Intent | Key differentiation | Pricing | G2 rating |

|---|---|---|---|---|---|

| 1 | Tapcheck | Best overall payroll-integrated EWA | No-code payroll and timekeeping integration, free for employers | Free for employers; employee per-transfer fee | 4.7/5 |

| 2 | Payactiv | Low-fee, financial wellness depth | No-fee ACH transfers plus budgeting and counseling | Free ACH; $2.49–$3.49 expedited | 4.5/5 |

| 3 | DailyPay | Brand recognition, engagement | Widely adopted on-demand pay with wellness tools | $0.00 listed | 4.7/5 |

| 4 | EarnIn | Consumer-style, no mandatory fees | Free standard Cash Out, optional faster delivery | $0 standard; paid faster options | 4.3/5 |

| 5 | Branch | Workforce payments plus wallet | Payouts plus digital banking app and card | $0 platform; some transfer fees | 4.7/5 |

| 6 | ZayZoon | SMB-friendly rollout | Free for employers, flat employee fee | Free to offer; $5.00 per transaction | 4.6/5 |

| 7 | Chime Workplace | Fee transparency | Fee-free for employers and employees | Free | 4.8/5 |

| 8 | Wisely® by ADP | Payroll-linked card workflows | Paycards and on-demand pay inside ADP | Not publicly listed | Not listed |

The 8 best earned wage access software platforms

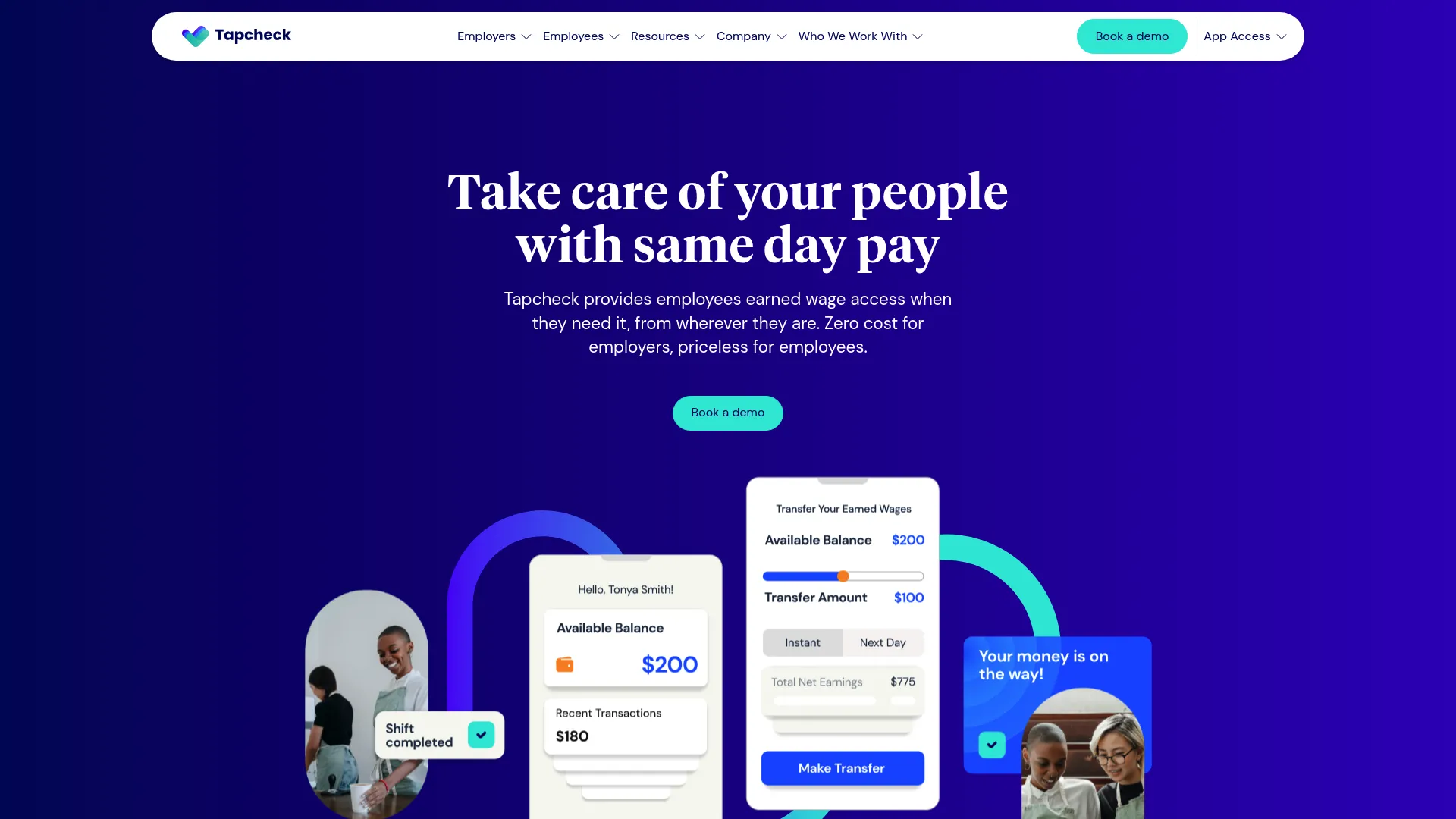

1. Tapcheck

Best for: Employers seeking earned wage access and on-demand pay with strong payroll integration and hands-off administration.

Key strengths

- No-code payroll and timekeeping integration: Connects to your existing systems without engineering work, so eligibility and balances stay accurate.

- Up to 70% of net earnings available: Employees can access a meaningful share of net pay right after a shift.

- Multiple disbursement and transparency options: Direct deposit, a Tapcheck Mastercard, and pay stub visibility give employees clarity on what they have earned.

Why choose Tapcheck: The combination of free employer cost and no-code payroll integration makes it the lowest-friction option for a fast, defensible rollout. You add a recruiting and retention benefit without a budget line or an integration project, which is exactly the profile an operator wants when justifying a new tool to a board.

Tapcheck pricing: Tapcheck's public pricing page lists employer cost as free, with the Employees plan, Small Business plan, and Enterprise plan all shown as free. Employees pay a single, ATM-like fee per transfer rather than a subscription. There is no employer subscription amount published.

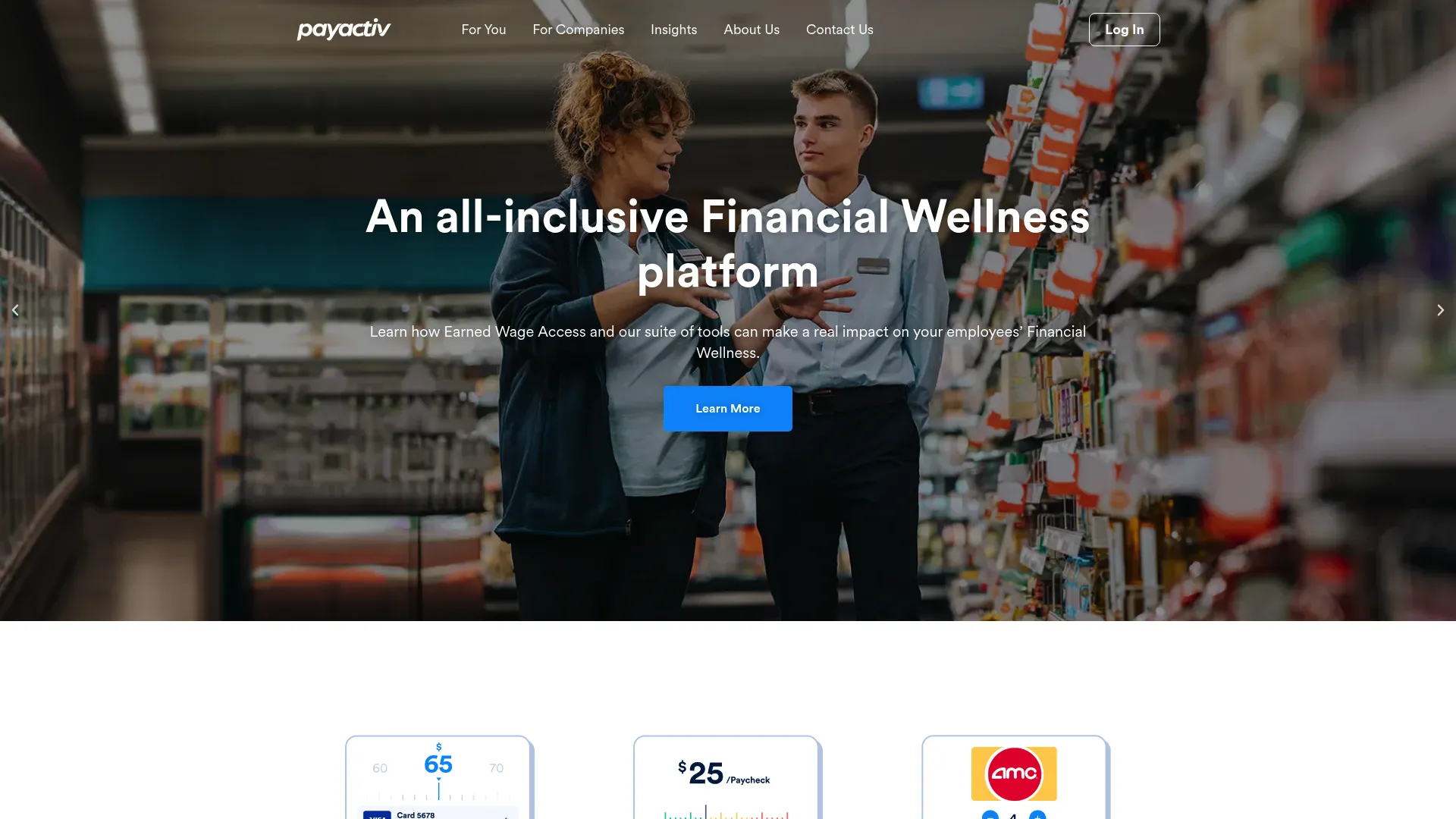

2. Payactiv

Best for: Employers seeking earned wage access plus a deeper set of employee financial wellness tools.

Key strengths

- No-fee transfer options: Standard ACH bank transfers carry no fee, and real-time transfers to a Payactiv Visa Card are free with qualifying direct deposit.

- Multiple disbursement methods: Bank transfer, Visa Card, bill pay, and cash pickup options give employees flexibility in how they access funds.

- Financial wellness layer: Budgeting, savings, discounts, and counseling extend the benefit beyond access alone.

Why choose Payactiv: If your turnover problem is rooted in broader financial stress rather than just timing, the wellness tools give employees more reasons to engage. The no-fee transfer path keeps the everyday experience friendly for workers who use it often.

Payactiv pricing: Payactiv publishes per-disbursement fees rather than subscription tiers. ACH bank transfers (1 to 3 business days) carry no fee. Real-time transfers to a Payactiv Visa Card are free with direct deposit of at least $200 per pay period, or $2.49 without it. Transfers to non-Payactiv debit cards, Walmart Cash Pickup, Venmo, and PayPal run $3.49.

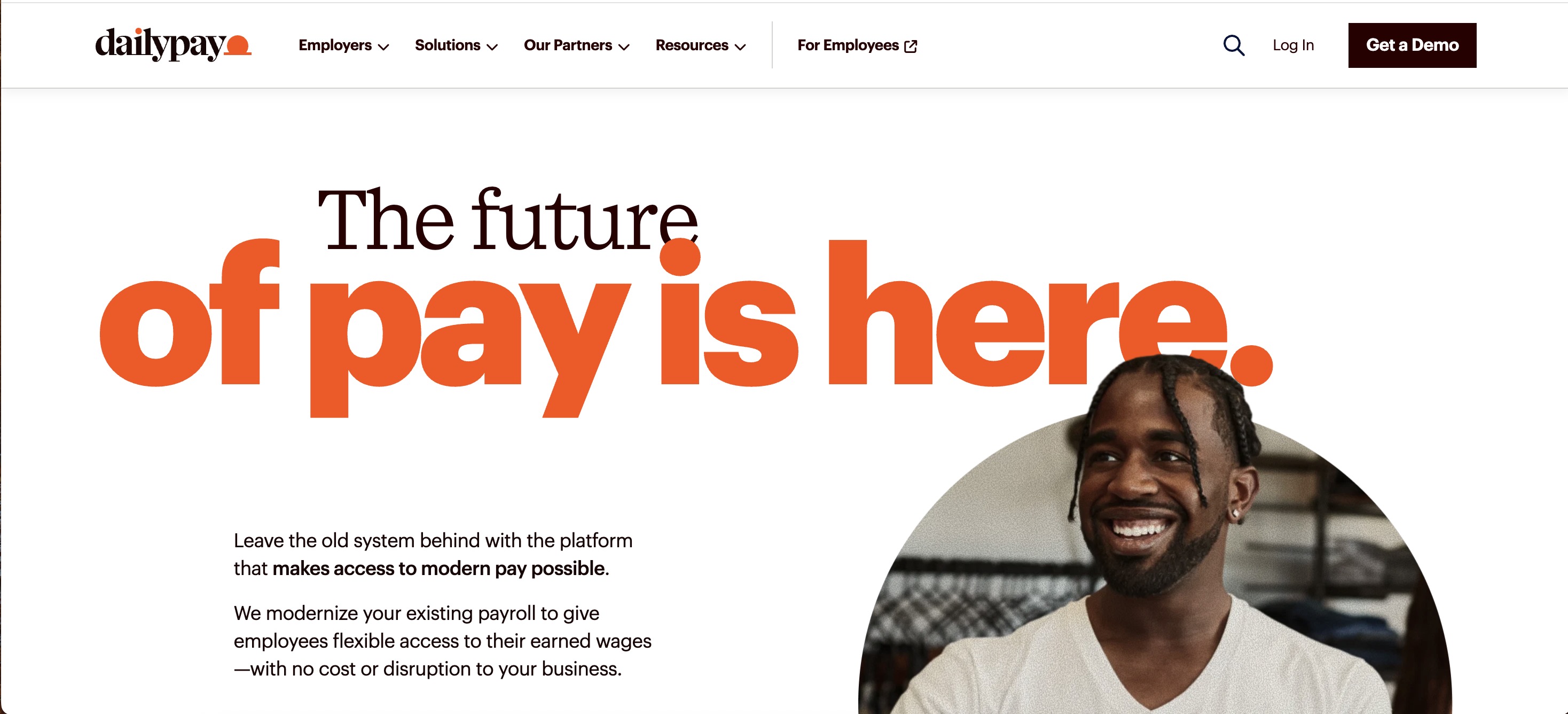

3. DailyPay

Best for: Employers who want a well-known on-demand pay platform with strong employee engagement and wellness features.

Key strengths

- Earned wage access with flexible delivery: Transfers route to a bank account, debit card, or pay card depending on employee preference.

- Financial wellness tools: Savings, credit monitoring, and bill management extend the value beyond access.

- Strong brand recognition: A widely adopted platform that employees may already know, easing adoption.

Why choose DailyPay: Brand recognition is an underrated rollout advantage. When employees already trust the name, fewer questions land on HR and adoption climbs faster. Pair that with the wellness tooling and you get an engagement-heavy benefit.

DailyPay pricing: DailyPay's public G2 listing shows the product at $0.00, and DailyPay's own site states that creating an account is free and there is no cost to receive remaining funds on payday. The employer-side product pricing is not published as a public subscription figure; employee-facing fees apply for certain expedited transfers.

4. EarnIn

Best for: Workers and employers who want earned wage access before payday without mandatory fees.

Key strengths

- Free standard transfers: Cash Out standard transfers cost $0, with optional Lightning Speed for faster delivery.

- Early Pay and Card options: Early Pay can route direct deposit up to two days early, and the EarnIn Card offers Live Pay access to earnings in real time.

- Built-in financial visibility: Balance Shield low-balance alerts and free credit monitoring with VantageScore 3.0 help workers manage cash flow.

Why choose EarnIn: The no-mandatory-fee model removes a common objection from employees who resent paying to access their own money. For workers who only occasionally need early access, the free standard path keeps it genuinely low cost.

EarnIn pricing: Standard Cash Out transfers are free. Lightning Speed faster delivery starts at $3.99. Early Pay expedited transfers cost $2.99. The EarnIn Card runs $2.99/month on autopay, or $12.99/month plus a $5 processing fee on manual pay. Cash Out is capped at $150/day with a $1,000 maximum per pay period.

5. Branch

Best for: Businesses that need faster worker payouts plus embedded workforce payments and banking features.

Key strengths

- Fast payouts to workers and contractors: Move funds quickly to both employees and contractors, not just W-2 staff.

- Branch App and Card: A digital wallet with a debit card gives workers a full financial account, not just access.

- Branch Direct payouts: Send funds directly to a worker's existing bank account when they prefer it.

Why choose Branch: If your payment needs extend past standard payroll into contractor payouts and instant disbursements, Branch handles more of the workflow in one place. The wallet and card ecosystem gives workers a banking experience on top of access.

Branch pricing: Branch states the platform is available at no cost to companies, with free options for workers. Some transfer fees apply: Branch Direct runs 2% of the transaction amount with a $2.99 minimum, and instant transfers to consumer accounts range from $2.99 to $4.99 depending on the transfer.

6. ZayZoon

Best for: Employers wanting a free-to-offer earned wage access benefit for hourly or deskless teams.

Key strengths

- Free for employers to offer: No cost to the company makes the rollout decision easy for a small business.

- Flat, predictable employee fee: A single $5.00 per transaction fee keeps the employee experience simple and transparent.

- Perks and recognition: Money-saving perks plus rewards and recognition extend the benefit beyond access.

Why choose ZayZoon: The flat fee and free-to-offer model strip out the complexity that slows SMB rollouts. You get a benefit you can explain in one sentence and launch without a procurement cycle, which matters when you do not have a dedicated benefits team.

ZayZoon pricing: ZayZoon is free for employers to offer. Employees pay a flat $5.00 fee per transaction for wage access. There is no broader public subscription pricing; the model is intentionally simple.

7. Chime Workplace

Best for: Employers seeking a no-cost financial wellness benefit for both employees and the company.

Key strengths

- Fee-free earned wage access: No cost to employees or employers removes the most common objection to the category.

- Savings and credit-building tools: Employees get help building financial health, not just accessing pay.

- Employer reporting: Workforce financial insights give employers a read on adoption and impact.

Why choose Chime Workplace: When fee transparency is the concern, a genuinely fee-free model is the strongest answer. The employer reporting also helps you defend the benefit internally with adoption data rather than anecdotes.

Chime Workplace pricing: Chime Workplace is publicly listed as free, with no cost to employers or employees. There is no detailed public pricing table beyond the free positioning.

8. Wisely® by ADP

Best for: Employers looking to move payroll to digital pay options and support financial wellness inside the ADP stack.

Key strengths

- Paycards and virtual paycards: Pay employees digitally, including workers without traditional bank accounts.

- Financial wellness tools: Support employee financial health alongside the pay mechanics.

- Off-cycle and on-demand payment support: Handle off-cycle pay and on-demand access within existing ADP workflows.

Why choose Wisely® by ADP: If you already run payroll on ADP, keeping digital pay and wage access inside the same ecosystem reduces vendor sprawl and integration overhead. The native fit is the advantage; you are not bolting on a separate system.

Wisely® by ADP pricing: ADP's public Wisely pages describe capabilities but do not expose public pricing. Pricing is handled through ADP directly, in line with how the broader payroll suite is sold.

Considerations before you buy

Use this checklist to pressure-test any earned wage access provider before committing. The right answers depend on your workforce, your payroll setup, and your tolerance for compliance exposure.

Payroll, HRIS, and timekeeping integration

The integration is the product. Confirm the provider connects cleanly to your specific payroll provider, HRIS, and timekeeping system, ideally with no-code setup. Weak integration means manual reconciliation and inaccurate available-balance calculations, which erodes employee trust fast. Ask exactly which systems are supported and how deductions are reconciled back into your payroll run.

Fee structure and transparency

Map out who pays what. Some providers are free to employers and employees; others charge per-transfer, instant-transfer, or card fees. Predictable, transparent fees protect both the employee experience and your reputation as the employer offering the benefit. Watch for fees that quietly shift cost onto your lowest-paid workers.

Compliance posture

Compliance depends on the funding model, fee structure, and state laws. Some structures stay clear of lending regulations like Regulation Z and TILA; others sit closer to the line, which has drawn CFPB attention. Ask the provider directly how their model is structured and which state requirements they handle. This is the part you do not want to discover after launch.

Employee experience and adoption

A benefit nobody uses is not a benefit. Look at the actual app: how fast a transfer lands, how clearly the available balance shows, and whether budgeting or savings features add value. High adoption is what turns EWA into a real retention and recruiting lever.

Speed to launch and admin overhead

For a small business or a lean team, implementation speed and ongoing administration matter as much as features. Favor providers that launch in days, run with minimal admin, and explain themselves to employees in a sentence.

Conclusion

Earned wage access is one of the rare benefits that can lift recruiting and retention without adding a budget line, because many providers are free to the employer. The right pick depends on your workforce and payroll setup.

For most employers, Tapcheck is the strongest overall choice thanks to no-code payroll integration and free employer cost. If you want deeper financial wellness alongside access, Payactiv delivers it with no-fee transfer options. DailyPay leads on brand recognition and engagement, while EarnIn fits workers who want access with no mandatory fees. Branch suits businesses with broader payout and banking needs, ZayZoon is the cleanest SMB rollout, Chime Workplace owns fee transparency, and Wisely® by ADP fits teams already on ADP.

Your next step: match your payroll provider against each vendor's integration list, then shortlist the two that fit your workforce size and run a 60-day pilot. Treat adoption rate as the metric that tells you whether it earned its place in your stack.

For more category breakdowns to inform your operational stack, browse guides like affiliate marketing software, ai content creation tools, and ai design tools.

FAQs

Earned wage access software is a payroll-linked platform or app that lets employees access wages they have already earned before their scheduled payday. It connects to your payroll, HRIS, and timekeeping data to calculate available earnings, then makes a portion accessible on demand through an employee-facing app.

For practical purposes, yes. On-demand pay, early wage access, and instant pay are terms vendors use interchangeably with earned wage access. They all describe accessing wages already earned before the normal pay cycle closes. When you compare providers, treat the labels as synonyms and focus on the fee structure and integration instead.

The platform integrates with your payroll provider and timekeeping system to read hours worked and calculate how much an employee has earned in real time. Employees access a share of that balance through the app, and the amount is reconciled back through deductions on the next payroll run. The cleaner the payroll integration, the less manual work lands on your team.

Common fees include instant-transfer fees, standard transfer fees (often free), card fees, and per-transaction fees. Some providers are free to both employer and employee, while others charge employees a flat or expedited fee. Transparency matters because hidden or stacked fees fall hardest on lower-paid workers and damage trust in the benefit.

No. A payday loan is a high-interest advance against future pay that must be repaid with fees and interest, often trapping borrowers in a cycle. Earned wage access gives employees money they have already earned, with no interest and typically no credit check on the access. The repayment is simply a deduction from wages already worked, not new debt.

Focus on payroll integration with your specific system, transparent fees, a clean employee experience, and speed to launch. A small business benefits most from providers that are free to offer, install with no-code integration, and require little ongoing administration. ZayZoon and Tapcheck are common SMB-friendly starting points.

Compliance depends on the provider's funding model, fee structure, and the state laws where your employees work. Some models stay clear of lending regulations like Regulation Z and the Truth in Lending Act, while others sit closer to the line and have drawn CFPB scrutiny. Ask each provider how their model is structured and which state requirements and deductions they handle before you commit.

For hourly and shift-based workforces, the factors that matter most are real-time timekeeping integration, fast transfer speed, and low or transparent employee fees. Tapcheck, Payactiv, and ZayZoon are all strong fits for hourly teams because they calculate available earnings from hours worked and keep the employee experience simple. The best choice depends on your payroll system and whether you want added financial wellness tools.