A shopper fills their cart, hits checkout, and stalls at the payment screen. The total feels too high to pay at once. They abandon. That moment repeats thousands of times a day across e-commerce, and buy now pay later software exists to close that gap by letting buyers split a purchase into installments without leaving your flow.

The category is no longer a niche bet. The global BNPL services market is forecast to reach USD 0.75 trillion in 2026, up from USD 0.65 trillion in 2025, growing at a 16.76% CAGR through 2031, according to Mordor Intelligence. Global BNPL users hit roughly 380 million in 2024 and are projected to climb to about 670 million by 2028, per Chargeflow. The demand is there. The harder question is which platform actually fits your stack.

That is where most buyers get stuck. BNPL software for merchants varies enormously in integration depth, compliance posture, deployment model, and whether it serves online checkout, in-store flows, or both. A consumer pay-in-4 brand and an enterprise issuing platform both call themselves BNPL, but they solve different problems for different teams. If you run a payments roadmap and care about repeatable revenue without operational drag, the wrong pick adds reconciliation headaches, compliance gaps, and engineering work you did not budget for.

This guide ranks 7 BNPL companies and platforms for 2026 through a merchant and payment-team lens, not a consumer-app lens. If you are evaluating tooling adjacent to your growth stack, you may also find our roundups of AI customer service software and affiliate marketing software useful as you map the broader checkout and acquisition picture.

What's inside

This guide is for merchants, payment teams, and financial institutions evaluating buy now pay later platforms. It covers seven options spanning consumer-facing BNPL brands, enterprise payment platforms, lending automation software, and a neutral review marketplace for shortlisting.

We selected tools based on four criteria that matter for buyers: integration depth (how cleanly it fits your checkout and back office), checkout flexibility (online, in-store, or both), compliance posture (KYC, AML, and risk ownership), and proof plus launch speed (customer evidence and time to go live). Pricing and ratings reflect verified, current values where publicly available.

TL;DR

- Best for financial institutions: Neofin, a no-code lending and BNPL automation platform.

- Best for enterprise configurability: OpenWay Way4, a real-time payments platform spanning issuing, acquiring, and BNPL.

- Best for category overview and buyer education: G2, the peer-review marketplace for shortlisting installment payment software.

- Best for consumer checkout brand recognition: Klarna, used by millions of shoppers online and in-store.

- Best for flexible pay-over-time experiences: Affirm, strong on higher-ticket financing.

- Best for pay-in-4 simplicity: Afterpay, available online, in-store, and in-app.

- Best for installment flexibility: Sezzle, with virtual-card checkout for use anywhere Visa is accepted.

If you are also reviewing tools for testing and optimizing your checkout funnel, our list of ab testing tools pairs well with this guide.

What is buy now pay later software?

Buy now pay later software is technology that lets merchants or lenders offer installment payments at checkout, so a shopper can split a purchase into scheduled payments instead of paying the full amount up front. The software handles the checkout integration, the approval decision, the payment schedule, and the settlement back to the merchant.

Not all BNPL software solves the same job. The category splits into a few distinct models, and knowing which one you need is half the buying decision.

- Split pay (pay-in-4): The shopper pays in equal installments, usually interest-free over six weeks. This is the model most consumers recognize and the one merchants reach for to lift checkout conversion.

- Installment lending: Longer repayment terms with interest, often used for higher-ticket purchases. This is closer to traditional financing and carries more compliance weight.

- Card-enabled BNPL: Installments delivered through a virtual or physical card, letting buyers pay over time anywhere the card network is accepted, not just at partner merchants.

- Omnichannel checkout: BNPL that works across online and offline checkout, including card-present and in-store scenarios, so the same financing option follows the customer.

Whatever the model, strong merchant BNPL software should give you a consistent set of capabilities. Buyers should expect:

- Clean integration with your existing checkout, payment gateway, and order management

- A fast, transparent approval flow that does not stall the buyer

- Installment scheduling and automated settlement with clear reconciliation

- Compliance support for KYC, AML, and risk checks where lending or cards are involved

- Reporting on approval rates, conversion, and repayment performance

- Support for online and offline checkout, plus BNPL integrations into your stack via API

The strongest checkout financing software treats these as table stakes. The differences show up in how deep the API goes, how much of the risk the provider owns, and whether the platform is built for a single merchant storefront or an entire financial institution issuing its own BNPL product.

When to use BNPL software

BNPL is not a universal fix. It earns its place in specific situations, and matching the tool to the moment matters more than picking the most recognized brand.

Launch BNPL at checkout

The clearest use case is lifting conversion at the payment step. When a meaningful share of your buyers abandon at checkout because the total feels too high, splitting that total into installments removes the friction. BNPL also tends to raise average order value, because buyers anchor on the installment amount rather than the full price. It performs best for financing-sensitive categories: apparel, electronics, furniture, healthcare, and other purchases where the sticker price gives shoppers pause.

Support online and offline sales

If you sell through more than one channel, omnichannel BNPL keeps the experience consistent. A buyer who discovers your installment option online should be able to use it in-store too. Card-enabled BNPL and card-present support extend the same financing into physical retail, in-app purchases, and point-of-sale terminals. This matters for merchants with hybrid models who do not want a financing option that only works on the website.

Replace fragmented payment plan workflows

Plenty of teams run informal payment plans through spreadsheets, manual invoicing, or one-off financing arrangements. That works until volume grows, then it becomes a reconciliation and compliance liability. Consolidating around a single BNPL platform replaces the patchwork with automated scheduling, settlement, and reporting. For financial institutions, installment payment software also centralizes underwriting, collections, and decisioning that would otherwise live across disconnected tools.

Comparison table

The seven options below span very different buyer profiles. Some are consumer-facing BNPL brands a merchant plugs into checkout. Others are platforms a bank or fintech uses to issue its own product. One is a review marketplace for shortlisting. Read the intent column first, because it tells you who each tool is actually built for.

| # | Product | Intent | Key use case | Pricing | G2 rating |

|---|---|---|---|---|---|

| 1 | Neofin | Financial institutions and lenders | No-code lending and BNPL automation | From $1,599/month | Not yet rated |

| 2 | OpenWay Way4 | Enterprise payment platforms | Issuing, acquiring, and BNPL at scale | Quote-based | 4.5/5 |

| 3 | G2 | Buyers shortlisting software | Peer reviews and vendor comparison | Free; Starter from $2,999/year | 4.6/5 |

| 4 | Klarna | Merchants and consumers | Flexible checkout, online and in-store | Merchant quote | 3.2/5 |

| 5 | Affirm | Merchants offering financing | Pay-over-time for higher-ticket items | Merchant quote | 4.2/5 |

| 6 | Afterpay | Merchants and shoppers | Pay-in-4, online, in-store, in-app | Free for on-time pay-in-4 | 4.1/5 |

| 7 | Sezzle | Merchants and shoppers | Installment checkout plus virtual card | Service fee $0 to $7.49 | 4.6/5 |

The pattern is clear: the right pick depends on whether you are a merchant adding a checkout option, a platform team building infrastructure, or an institution issuing your own BNPL product. Pricing transparency tracks with that split too. Consumer-facing brands quote merchants directly, while platform software publishes subscription tiers or stays quote-based.

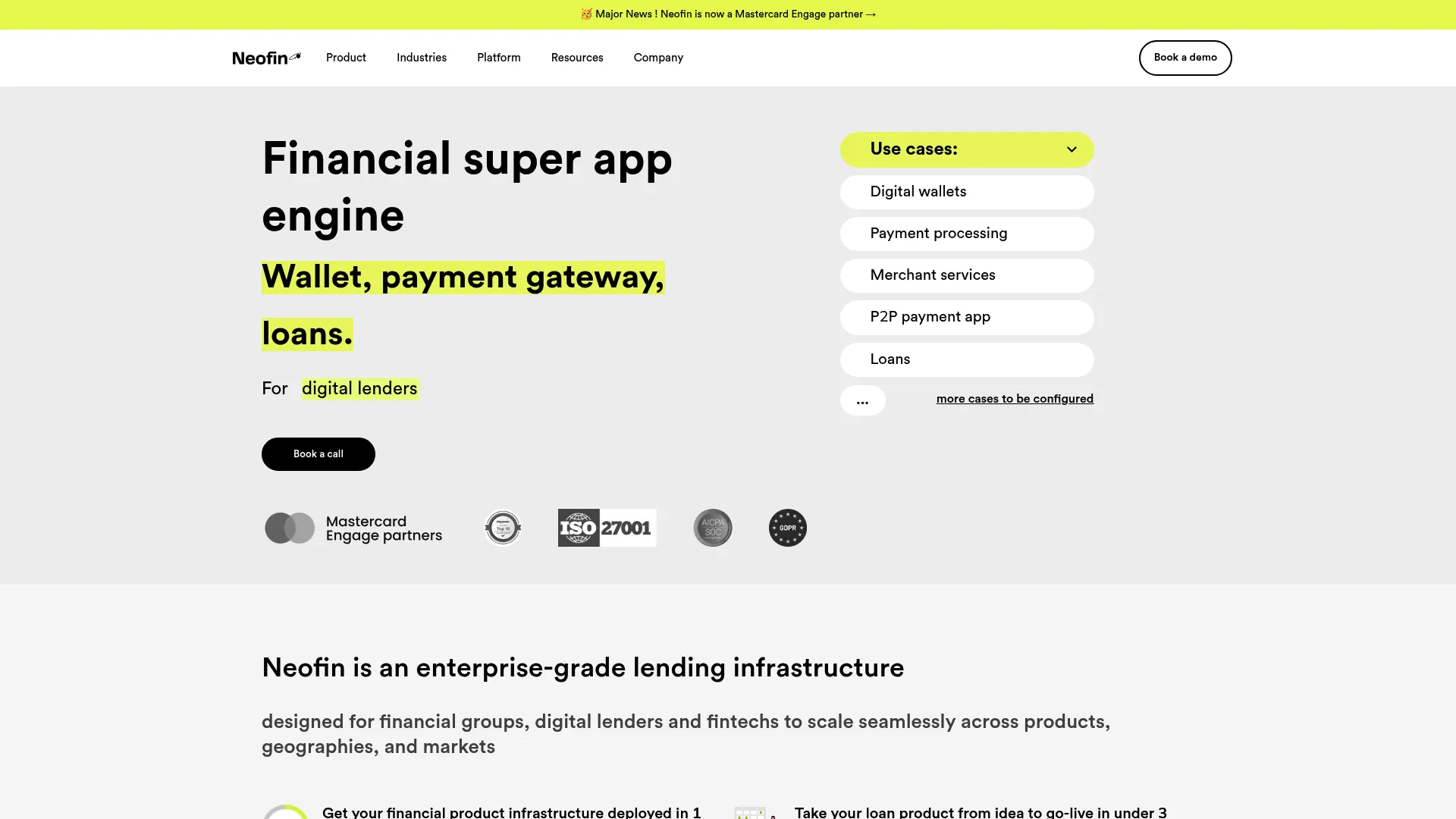

1. Neofin

Neofin is a no-code credit and lending automation platform built for teams launching and managing loan and BNPL products. It targets lenders, fintechs, and financial institutions that want to stand up an automated loan lifecycle quickly, without building origination, servicing, and collections from scratch. BNPL is one of the modules available within its broader lending stack, which makes it a fit for institutions issuing their own pay-over-time product rather than merchants plugging a brand into checkout.

Best for: Lenders and fintech teams launching automated loan or BNPL products quickly.

Key strengths

- No-code loan automation: Build and manage loan workflows, decisioning, and BNPL flows through a visual builder rather than custom engineering.

- Full loan lifecycle coverage: Origination, servicing, collections, and decisioning live in one platform, reducing the tool sprawl institutions often inherit.

- Deep integrations: Connects with core banking systems, CRMs, payment gateways, and external data sources for KYC, AML, and scoring.

Why choose Neofin: If you are a financial institution or fintech that wants to own the BNPL product end to end, including underwriting and compliance, Neofin gives you the infrastructure without a multi-year build. The no-code layer matters for teams that want product and risk staff configuring flows instead of waiting on engineering. It is the issuer-side counterpart to the consumer brands further down this list.

Neofin pricing: Neofin uses a mixed subscription plus pay-as-you-go model. The Basic plan starts from $1,599 per month and includes core loan lifecycle modules. The Premium plan adds advanced modules such as BNPL, POS, KYC, AML, scoring, and collections strategies on a pay-as-you-go basis on top of Basic. A free tier is available. Neofin currently shows no G2 review volume, so there is no established rating to weigh yet.

2. OpenWay Way4

OpenWay Way4 is OpenWay's real-time digital payments platform for issuing and accepting payment instruments across cards, wallets, switching, acquiring, BNPL, and digital banking. It is built for tier-1 banks, processors, and fintechs modernizing payment infrastructure, and it treats BNPL as one capability inside a much larger payments engine. Way4 supports both greenfield launches and complex migrations at scale, which is why it shows up in enterprise payment roadmaps rather than single-merchant checkout setups.

Best for: Tier-1 banks, processors, and fintechs modernizing payment issuing and acquiring.

Key strengths

- Full payments coverage: Card issuing, acquiring, switching, wallets, an e-commerce gateway, and omnichannel digital banking in one platform.

- No-code configuration: Automation and rule-based pricing, limits, and workflows let teams adjust products without rewriting code.

- Flexible deployment: Cloud, SaaS, and on-premises options with multi-country support for global operations.

Why choose OpenWay Way4: If your BNPL ambitions sit inside a broader issuing and acquiring strategy, Way4 gives you configurability and deployment depth that consumer brands cannot. Tokenized payments, rule-based limits, and omnichannel support make it suited to institutions that need card-enabled and non-card BNPL under one roof, with compliance considerations handled at the platform level. It is the heavyweight pick for platform and issuer teams that need flexibility above all.

OpenWay Way4 pricing: OpenWay does not publish public pricing for Way4. Pricing appears to be quote-based and tied to deployment scope, so expect a sales conversation rather than a published tier. On G2, Way4 holds a 4.5/5 rating, though review volume is currently limited.

3. G2

G2 is the B2B software marketplace and peer-review platform, not a BNPL provider itself. We include it here as a neutral comparison anchor rather than a product recommendation, because shortlisting installment payment software is a real part of the buying process and G2 is where many buyers do that work. Its peer reviews, comparison filters, and the Grid evaluation model help you read the market before you commit to vendor demos.

Best for: Teams buying or marketing B2B software that want peer reviews and market-intelligence-driven vendor discovery.

Key strengths

- Peer-to-peer reviews: Verified user reviews give you implementation and support signal that vendor pages do not.

- The Grid model: A visual evaluation framework that maps vendors by satisfaction and market presence at a glance.

- Comparison and filtering: Side-by-side feature, pricing, and segment filters to narrow a long list of buy now pay later platforms fast.

Why choose G2: When you are early in the evaluation and need to separate marketing claims from real user experience, G2 is the fastest way to build a shortlist. It will not process a payment, but it helps you decide which of the providers on this list deserve a deeper look based on how teams like yours rate integration depth, support, and reliability.

G2 pricing: G2's marketplace listings are free to browse for buyers. For vendors marketing on the platform, G2 Marketing Solutions starts at $0 for a Free edition, with a paid Starter tier from $2,999 per year and higher Professional and Enterprise tiers available on request. G2 holds a 4.6/5 rating on its own platform.

4. Klarna

Klarna is one of the most recognized names in consumer BNPL, offering flexible pay-later options, cashback, and app-based money management. It is the preferred payment option for both brands and customers, used by millions of shoppers every month, online and in-store. For merchants, that brand recognition is the draw: shoppers already know and trust the Klarna button at checkout, which lowers hesitation at the payment step.

Best for: Consumers and merchants looking for flexible checkout and BNPL-style payment options.

Key strengths

- Flexible payment options: Interest-free installments alongside longer pay-over-time plans give shoppers a familiar set of choices.

- Cashback and app engagement: Purchases through the Klarna app earn cashback, which keeps shoppers returning through Klarna's surface.

- Klarna Card and money management: App-based tools extend the relationship beyond a single checkout into ongoing financial management.

Why choose Klarna: If shopper recognition and conversion at checkout are your priorities, Klarna's brand does heavy lifting. Merchants choose it because the option is already familiar to a large consumer base, reducing the education needed at the payment screen. It fits a checkout strategy built around consumer trust and a broad existing user base across online and offline channels.

Klarna pricing: Klarna does not publish a standalone merchant pricing table on its public site. Like most consumer BNPL brands, merchant pricing is arranged directly and typically tied to transaction volume and structure, so expect a commercial conversation. On G2, Klarna holds a 3.2/5 rating.

5. Affirm

Affirm is a buy now pay later and pay-over-time financing platform serving both shoppers and merchants. It leans toward flexible, longer-term payment plans and is a common choice for higher-ticket purchases where a six-week split is not enough runway for the buyer. Affirm emphasizes transparency: shoppers see the terms up front, and eligible purchases can carry 0% APR, which helps merchants frame financing as a benefit rather than a cost.

Best for: Merchants that want to offer BNPL financing at checkout, especially for higher-ticket items.

Key strengths

- Flexible pay-over-time plans: Longer repayment terms suit electronics, furniture, travel, and other higher-value categories.

- 0% APR options: Eligible purchases can carry no interest, which merchants can use to drive conversion on big-ticket items.

- Merchant checkout integrations: Financing plugs into the checkout flow with integrations built for online merchants.

Why choose Affirm: When your average order value is high enough that buyers need more than a pay-in-4 window, Affirm's longer terms fit better. The transparent terms and 0% APR options make it a strong conversion lever for considered purchases, and the merchant integrations keep the financing decision inside your checkout. It is the pick for merchants optimizing conversion on higher-ticket carts.

Affirm pricing: Affirm does not publish merchant pricing on its site. A merchant FAQ notes that a typical fee is a base percentage plus a fixed amount per transaction, varying by business type and size, so the exact rate comes through a sales conversation. On G2, Affirm holds a 4.2/5 rating.

6. Afterpay

Afterpay is a buy now pay later service for shoppers and merchants built around pay-in-4 simplicity. The core offer is four interest-free installments over six weeks, a model that is easy for shoppers to understand and easy for merchants to explain. Afterpay also works online, in-store, and in-app, and offers longer Pay Monthly terms for eligible U.S. users, broadening it beyond pure split-pay.

Best for: Shoppers and retailers seeking a BNPL payment option with online, in-store, and app-based checkout.

Key strengths

- Pay in 4 interest-free: Four installments over six weeks, free when paid on time, is the clearest BNPL proposition for shoppers.

- Pay Monthly options: Eligible U.S. users can pay over 3, 6, 12, or 24 months, extending beyond split-pay for larger purchases.

- Omnichannel acceptance: Works online, in-store, and in-app, so the option follows the customer across channels.

Why choose Afterpay: Merchants often choose Afterpay because the pay-in-4 model is the easiest BNPL option to communicate, which reduces friction at checkout. The simplicity drives conversion without requiring shoppers to evaluate interest rates or long terms. Add omnichannel acceptance and it fits retailers selling across web, app, and physical store.

Afterpay pricing: For shoppers, Afterpay's Pay in 4 is free when paid on time at partnered merchants, with late fees possible. Pay Monthly carries APRs from 0.00% to 35.99% depending on eligibility and merchant. Merchant-side pricing is described as simple and transparent but is not published as a numeric fee, so merchants should request a quote. On G2, Afterpay holds a 4.1/5 rating.

7. Sezzle

Sezzle is a buy now pay later platform offering installment checkout and a virtual-card option. It supports Pay in 2, Pay in 4, and Pay Monthly plans, plus Sezzle Anywhere, a virtual card that works anywhere Visa is accepted. That card-enabled angle is its differentiator: rather than limiting financing to partner merchants, Sezzle lets shoppers extend installment payments across a much wider set of purchases.

Best for: Shoppers and merchants looking for BNPL installment payments and virtual-card checkout.

Key strengths

- Multiple installment plans: Pay in 2, Pay in 4, and Pay Monthly cover different cart sizes and shopper preferences.

- Sezzle Anywhere virtual card: A virtual card usable anywhere Visa is accepted extends BNPL beyond partner merchants.

- Online and in-store support: Checkout works across web and physical retail, fitting hybrid merchants.

Why choose Sezzle: Relative to the largest BNPL brands, Sezzle competes on installment flexibility and the card-enabled reach of Sezzle Anywhere. For merchants who want a BNPL partner with strong installment options and shoppers who value paying over time anywhere Visa works, it is a practical alternative to the household names. It fits merchants prioritizing flexible terms and broad usability.

Sezzle pricing: Sezzle states that service fees vary by purchase price and product, with examples ranging from $0 to $7.49 per transaction. A separate subscription fee applies to Sezzle Anywhere, though the exact amount is not publicly listed. Pay Monthly pricing is also not publicly specified. On G2, Sezzle holds a 4.6/5 rating.

What to evaluate before you buy

The shortlist above spans very different buyer types, so the right evaluation depends on whether you are a merchant, a platform team, or an institution. A few criteria apply across all of them.

Integration depth and API fit

Look at how the BNPL software connects to your checkout, payment gateway, and order management. API-based BNPL with documented endpoints and prebuilt integrations into your stack will launch faster than a bolt-on widget that needs custom glue code. For platform teams, check whether the API supports the events and webhooks your reconciliation depends on.

Compliance and risk ownership

Decide who owns BNPL risk and compliance. Consumer brands like Klarna, Affirm, Afterpay, and Sezzle typically own the underwriting and the consumer relationship, which keeps your compliance burden lighter. Platforms like Neofin and OpenWay Way4 let you own the product, which means you own more of the KYC, AML, and lending compliance too. Match this to your appetite and your regulatory standing.

Online and offline coverage

Confirm whether the platform supports online and offline checkout. If you sell in physical stores, card-present or card-enabled BNPL matters. A web-only option leaves your in-store conversion untouched.

Reporting and reconciliation

Check what reporting you get on approval rates, conversion lift, settlement timing, and repayment performance. Clean reconciliation is what keeps BNPL from becoming a finance-team headache as volume grows.

Launch speed and proof

Weigh time to go live and the customer proof behind each option. Ask for references in your segment and verify the integration timeline before signing.

Conclusion

The seven options here serve genuinely different buyers, and that is the most important takeaway. If you are a financial institution or fintech issuing your own pay-over-time product, Neofin gives you no-code lending and BNPL automation across the full loan lifecycle. If your BNPL ambitions sit inside enterprise issuing and acquiring, OpenWay Way4 brings the configurability and deployment depth. G2 is where you go to shortlist and read peer signal before committing.

On the merchant side, the choice comes down to fit. Klarna leads on consumer recognition, Affirm on flexible pay-over-time financing for higher-ticket carts, Afterpay on pay-in-4 simplicity across channels, and Sezzle on installment flexibility plus card-enabled reach through Sezzle Anywhere.

The right merchant BNPL software depends on whether you are an issuer, a platform, or a merchant. Shortlist two or three options that match your model, validate the BNPL integrations against your actual checkout and back office, then compare compliance posture and rollout speed side by side. That sequence keeps the decision grounded in your stack rather than the loudest brand. As you build out the surrounding toolkit, our guides to ai content creation tools and ai design tools can help round out the checkout and marketing experience around your payment plans.

FAQs

Buy now pay later software is technology that lets merchants or lenders offer installment payments at checkout, so shoppers split a purchase into scheduled payments instead of paying in full up front. Models vary by term length, who owns the credit risk, and how deeply the software integrates with your checkout. Some are consumer-facing pay-in-4 brands, while others are full lending platforms financial institutions use to issue their own product.

For merchants, the software integrates into the checkout, presents a financing option, runs a real-time approval decision, and sets up the installment schedule for the shopper. Once approved, most consumer BNPL providers pay the merchant the full amount up front and take on the repayment collection themselves. The merchant then reconciles settlements and reporting through the provider's dashboard or API, which is why integration depth and reconciliation quality matter so much.

The terms overlap, but there is a useful distinction. BNPL is usually shopper-facing and checkout-centric, optimized to lift conversion at the payment step with short, often interest-free terms. Installment payment software is a broader category that can include longer repayment structures, full lending workflows, underwriting, and collections, which is what financial institutions need when they issue their own pay over time software rather than plugging in a consumer brand.

Prioritize integration quality with your checkout and gateway, a fast and transparent approval flow, compliance posture, clear reporting, and support for online and offline checkout. Tie each of these back to two outcomes: how quickly you can launch and how much the option lifts conversion. A platform that is slow to integrate or weak on reconciliation will erode the conversion gains it promises.

It depends on the model. Consumer pay-in-4 providers typically own the identity and risk checks themselves, keeping your BNPL compliance burden lighter. When cards or lending products are involved, or when you issue your own BNPL through a platform, issuer-level KYC and AML checks become your responsibility. Confirm who owns the checks before you commit, because it changes your operational and regulatory load significantly.

Yes, if the platform supports omnichannel or card-enabled flows. Brands like Afterpay and Sezzle support in-store and in-app checkout, and card-enabled BNPL such as Sezzle Anywhere extends financing anywhere the card network is accepted. Offline acceptance broadens the use case well beyond e-commerce, which matters for hybrid retailers who want the same financing option across web and physical store.

Pricing for buy now pay later platforms comes in three flavors: published subscription tiers, quote-based merchant pricing, and consumer-fee structures tied to transaction value. Platform software like Neofin publishes a starting monthly price, while most consumer brands quote merchants directly based on volume and structure. When you evaluate, check setup fees, per-transaction fees, merchant discount rates, and any subscription components, and confirm how settlement timing affects your cash flow.