You decided to offer a lifestyle benefit. Good call. Then the reimbursements started, and the spreadsheet you built to track them broke by month two.

Here is the pattern almost every team hits. Offering flexible, employer-funded benefits is easy to announce. Administering them is not. The moment eligibility rules, receipts, tax treatment, and payroll adjustments enter the picture, manual tracking stops scaling. Someone on your people team spends Friday afternoons cross-checking gym receipts against a policy document nobody remembers writing.

That is the problem lifestyle spending account software solves. And the timing matters. Only 10% of companies currently offer a lifestyle spending account, with adoption more than doubling since 2024, according to Sequoia's 2025 data. Meanwhile 66% of employers said they were considering LSAs in a 2024 Gallagher and IFEBP survey. The category is moving from novelty to standard benefit, and the software you pick decides whether that program feels effortless or turns into an admin tax.

This shortlist is built for operators choosing an LSA platform, not a definition of what an LSA account is. If you are still validating whether an interactive demo of a benefits tool matches your workflow, or comparing adjacent stack pieces like account-based marketing software or a customer data platform, those live elsewhere. Here we rank nine tools by how cleanly they handle the real work: reimbursement workflow, compliance, and employee experience.

What's inside

This guide covers lifestyle spending account software for employer-funded, post-tax benefit programs. It is written for HR, people ops, finance, and benefits buyers who have already decided to offer an LSA and now need software to run it without manual receipt chasing.

We selected and ranked the nine platforms on five criteria that decide day-to-day admin effort: reimbursement workflow quality, eligibility and customization controls, compliance and tax support, reporting and payroll integration, and employee experience. Pricing and G2 ratings reflect verified, publicly available values. Where a vendor gates pricing behind a sales conversation, we say so rather than guess.

TL;DR

- Best for reimbursement-first programs: Compt automates stipend and LSA reimbursements with payroll-ready reporting, so receipts never route through a spreadsheet.

- Best for a modern card-and-reimbursement employee experience: Benepass pairs physical and virtual cards with reimbursements and a mobile wallet.

- Best for total rewards and engagement: Espresa combines lifestyle spending accounts with wellbeing, recognition, and community programs.

- Best for broader benefits administration: PeopleKeep leans into HRA administration with clear tax and compliance guidance.

- Best for consolidating perks, recognition, and lifestyle benefits: Fringe offers a marketplace-style employee experience with public per-employee pricing.

- Best for a simple, flexible LSA to launch fast: Joon starts at a flat monthly rate with customizable allowances and eligibility rules.

Background: what lifestyle spending account software does

Lifestyle spending account software is a benefits administration platform that lets employers fund, manage, and reimburse flexible lifestyle and wellness spending under an employer-defined set of eligible categories. An LSA account is employer-funded, and because it does not have the strict IRS rules of an FSA or HSA, employers get wide latitude over what counts as eligible, from gym memberships to childcare to home office gear.

The tradeoff for that flexibility is tax treatment. LSA funds are almost always treated as taxable income to the employee, which is why these programs run as post-tax reimbursements. Good LSA software handles that treatment automatically, feeding the taxable amount into your payroll so nobody reconciles it by hand.

Most lsa software falls into one of three operating models. Understanding which one you want is the single most useful decision before you compare features:

- Reimbursement-first: Employees pay, submit a receipt, and get reimbursed through payroll or direct deposit. Strongest for control, clean substantiation, and taxable-income handling.

- Card-based LSA: Employees spend on a funded physical or virtual card. Strongest for immediacy and employee experience, with merchant category controls doing the eligibility work.

- Marketplace or perks: Employees choose from a curated catalog of vendors and experiences. Strongest for engagement and curated choice.

Whatever the model, expect these core capabilities from a serious platform:

- Configurable eligibility rules and eligible-expense categories

- A clean reimbursement workflow with receipt capture and substantiation

- Automated tax treatment and payroll integration

- Employer customization of allowances, cadences, and program design

- Reporting for finance and compliance

- A self-serve employee experience on web and mobile

What to look for in lifestyle spending account software

Feature lists blur together fast. These are the criteria that actually change your monthly admin load.

Reimbursement speed and workflow. How fast does a claim go from submitted to paid, and how much of that path is automated? A reimbursement-first model lives or dies on this. Look for automated receipt review, clear approval logic, and direct payroll or deposit payouts.

Eligibility controls and customization. Because an LSA has no fixed IRS category list, your software has to enforce your policy. Check whether you can define categories, set allowances per group, and adjust rules without a support ticket every time.

Substantiation and compliance. Someone has to prove a purchase qualified. The platform should capture receipts, flag exceptions, and keep an audit trail. Compliance and tax treatment should be handled inside the tool, not offloaded to your finance team.

Payroll and HRIS integration. Because most LSA reimbursements are taxable, the taxable amount has to reach payroll accurately. Verify native connections to your payroll and HRIS stack, or clean export at minimum.

Reporting. Finance needs spend by category, utilization, and taxable totals on demand. Weak reporting turns quarter-end into a data-assembly project.

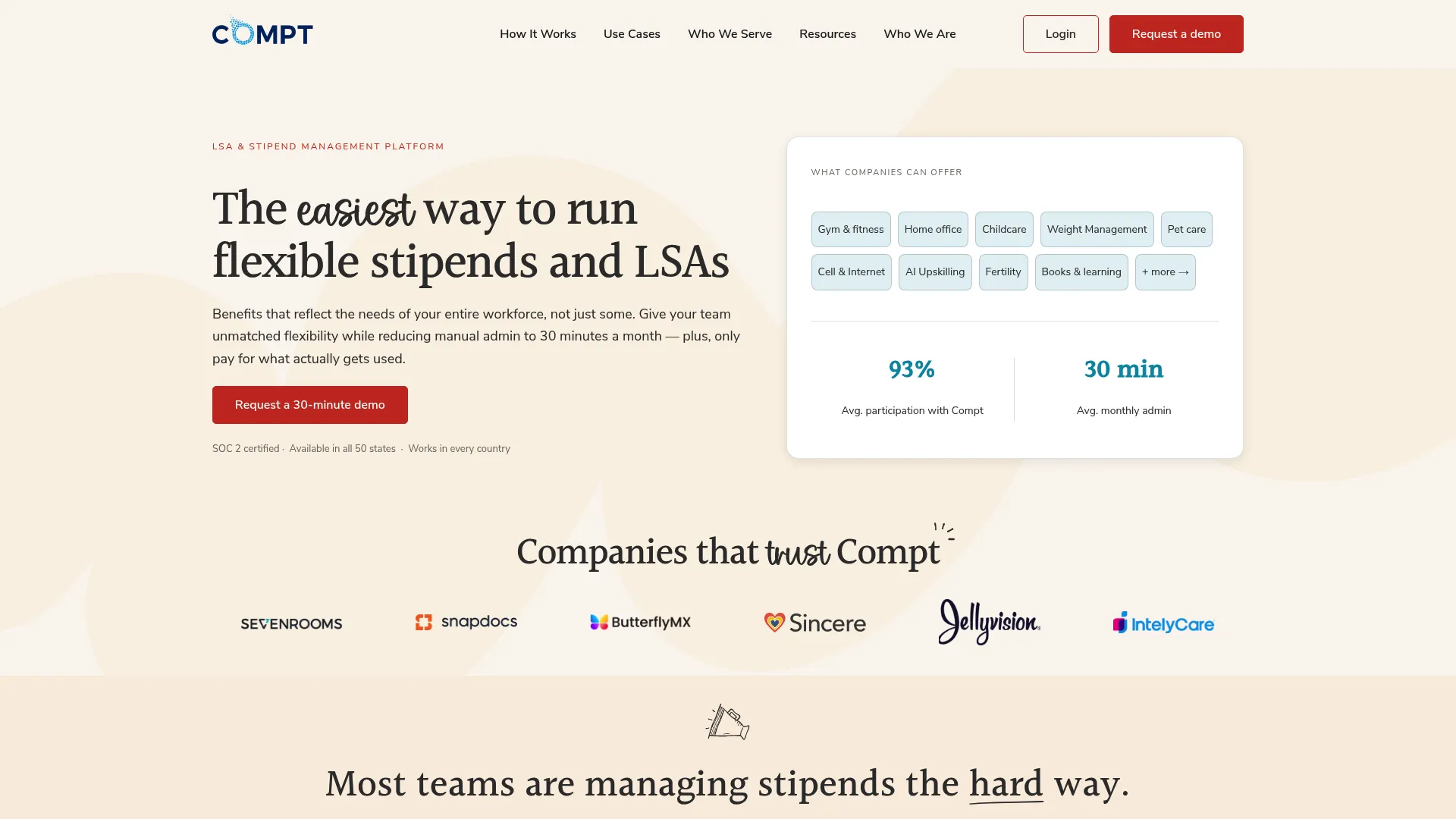

Employee experience. Adoption is the whole point. Among existing LSA programs, Compt's 2026 benchmark reports 93% employee participation and 89% of funds used. That kind of engagement depends on a benefit that is easy to understand and easy to claim.

When companies use lifestyle spending account software

Replacing manual reimbursements. The most common trigger. A perk started in a spreadsheet, grew past what one person can track, and now needs automation and an audit trail.

Launching a new wellness or lifestyle benefit. A team wants to offer employee wellness benefits and choice without inventing an admin process from scratch. Software gives them eligibility rules, payouts, and tax handling on day one.

Standardizing across teams or regions. Distributed and global teams need consistent employer-funded benefits with local reimbursement or card support, not a patchwork of one-off arrangements.

Reducing admin burden as you scale. For a founder or people lead watching headcount grow, the goal is a benefit that runs without a person in the loop for every claim. Consolidating onto one lifestyle spending account platform removes a recurring manual task and gives finance clean reporting.

Comparison table

Here is the shortlist ranked by relevance to reimbursement-first LSA buyers. Pricing reflects publicly available values; several vendors quote based on company size.

| # | Product | Intent | Key differentiation | Pricing | G2 rating |

|---|---|---|---|---|---|

| 1 | Compt | Reimbursement-first LSA | Automated stipend and LSA reimbursements with payroll-ready reporting | Custom / request a quote | 4.8/5 |

| 2 | Benepass | Card + reimbursement | Global physical and virtual cards plus mobile wallet | Not publicly listed | 4.8/5 |

| 3 | Espresa | Total rewards + LSA | Lifestyle accounts with wellbeing, recognition, and community | Not publicly listed | 4.2/5 |

| 4 | PeopleKeep | Benefits administration | HRA-focused administration with tax guidance | From $12/employee/mo | 4.4/5 |

| 5 | WEX | Enterprise benefits infra | Fleet, payments, and benefits infrastructure at scale | Contact WEX | Not verified |

| 6 | Fringe | Marketplace / perks | Consolidated rewards, wellbeing, and lifestyle marketplace | From $2/PEPM | 4.7/5 |

| 7 | ThrivePass | Wellness + pre-tax accounts | LSA plus FSA, HSA, HRA, and commuter accounts | From $0.55/mo (third-party) | 4.1/5 |

| 8 | Joon | Simple flexible LSA | Automated reimbursement with customizable allowances | From $250/mo | Not verified |

| 9 | BenefitHelp Solutions | Outsourced admin | FSA, HRA, COBRA, and reimbursement account services | Request a quote | Not verified |

1. Compt

Compt is a reimbursement-based platform for managing flexible stipends and lifestyle spending accounts. It is built around the idea that employees pay for what they want, submit a receipt, and get reimbursed cleanly through payroll, with the taxable treatment handled automatically. That reimbursement-first model is why it sits at the top of this list for control and cleanup.

Best for: HR teams that want to automate flexible stipends and LSAs without touching receipts manually.

Key strengths

- Automated reimbursement workflow: Receipts submitted, reviewed, and paid without a spreadsheet in the middle.

- Payroll-ready tax reporting: Taxable amounts flow into payroll, so post-tax reimbursements reconcile themselves.

- Flexible eligible categories: Employee self-service across a wide, employer-defined set of eligible expense categories.

Why choose Compt: If your priority is control, clean substantiation, and getting the taxable-income handling right, the reimbursement-first model does the heavy lifting. It removes the two things that break manual LSA programs: chasing receipts and reconciling taxable amounts at quarter-end. For a people team that wants the benefit to run without someone in every claim, this is the safest default.

Compt pricing: Compt does not publish a fixed public price. Pricing depends on company size and how stipends and LSAs are used, and the company asks prospects to request a quote. It describes a fixed annual tier model, and says every Lifestyle Benefits plan includes unlimited programs and built-in features. On G2, Compt holds a 4.8/5 rating.

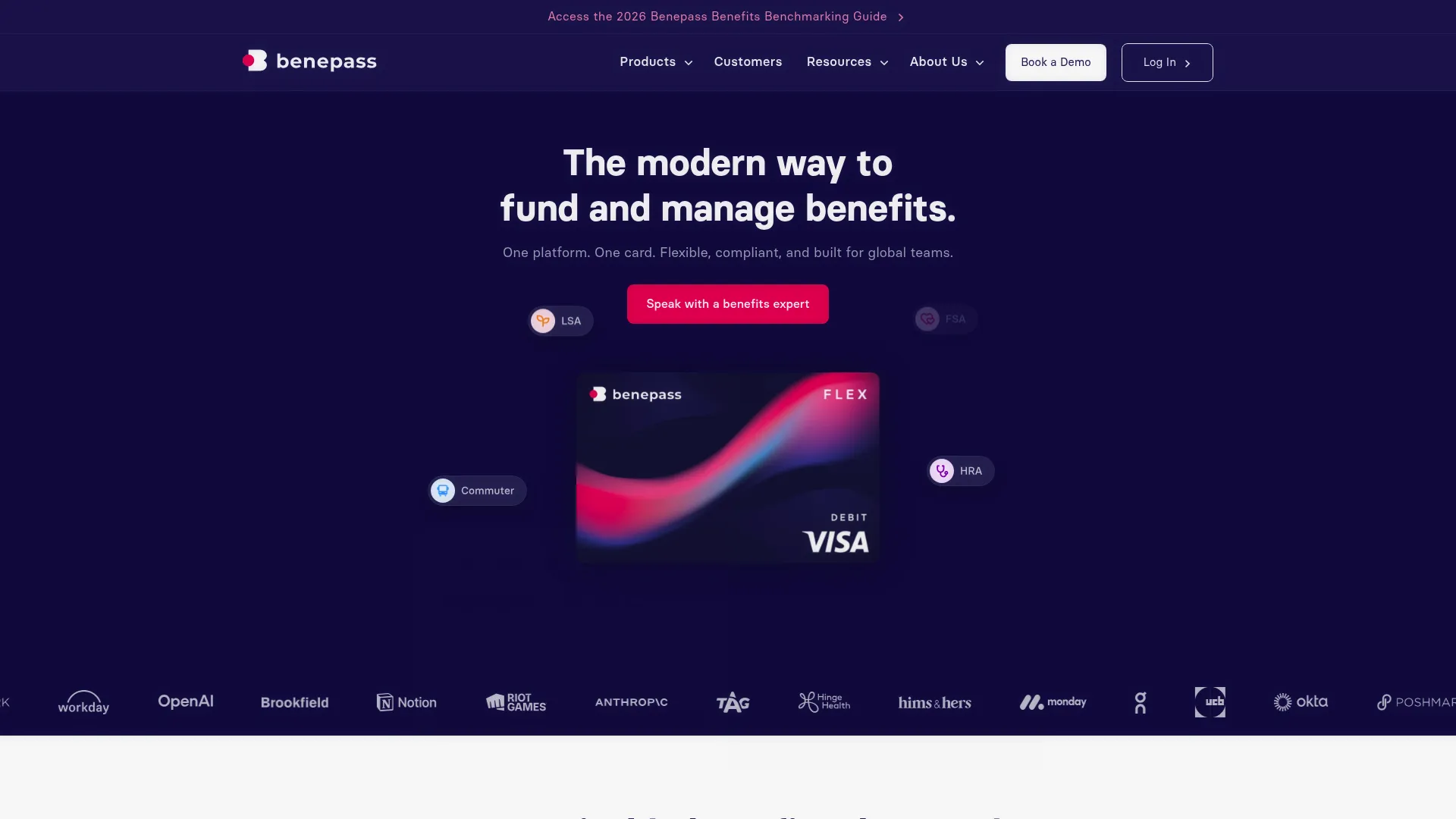

2. Benepass

Benepass is a flexible employee benefits platform for global teams that pairs card-based spending with reimbursements. Employees can spend on a physical or virtual card, tap a mobile wallet, or submit for reimbursement, which gives the program an immediate, modern feel. It sits second because that card-and-reimbursement combination fits teams that prioritize employee experience alongside control.

Best for: Employers offering flexible, globally usable benefits programs across multiple regions.

Key strengths

- Global cards: Physical and virtual cards that work across regions for distributed teams.

- Automated enrollment and tax compliance: Enrollment and compliance handled inside the platform.

- Reimbursements and mobile wallet: Employees choose how they spend, on card or by reimbursement.

Why choose Benepass: Card-based LSA spending removes the pay-then-wait step that reimbursement-only programs carry, which employees notice. If your team spans multiple countries and you want one flexible benefits platform rather than regional workarounds, Benepass is built for that footprint. It suits companies where the employee experience of the benefit is as important as the admin side.

Benepass pricing: Benepass does not publicly display pricing on its site, using demo and get-in-touch CTAs instead. On G2, Benepass holds a 4.8/5 rating.

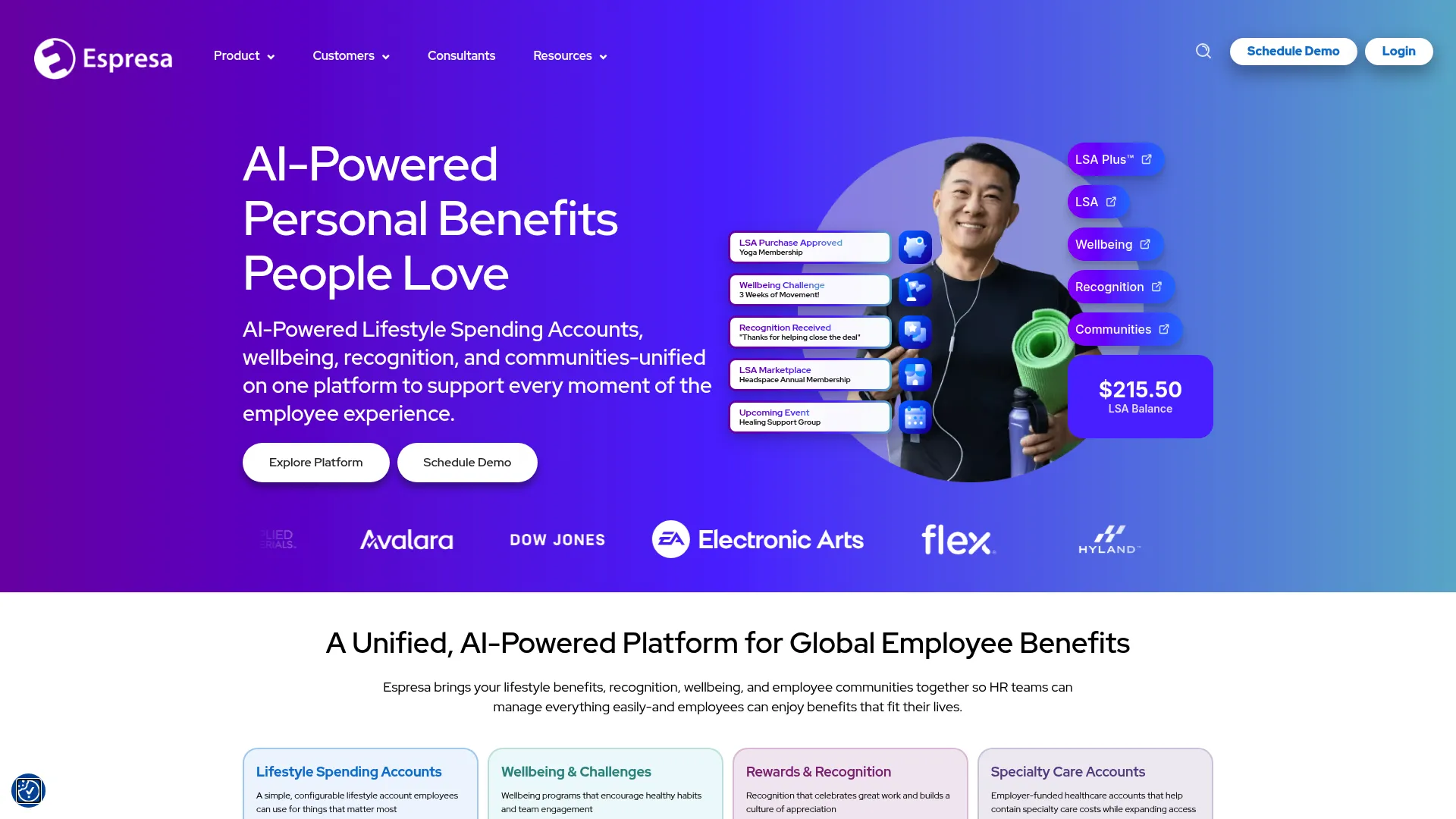

3. Espresa

Espresa is an AI-powered employee benefits platform that folds lifestyle spending accounts into a wider total rewards experience: wellbeing, recognition, communities, and specialty care. If you want the LSA to be part of an engagement story rather than a standalone reimbursement tool, this is the one to look at. It ranks third for teams building a broader rewards program.

Best for: Global HR teams managing benefits and engagement programs in one platform.

Key strengths

- AI Eligibility Adviser: Guidance that helps employees understand what qualifies without a support ticket.

- Global marketplace with 0% markup: A vendor marketplace employees browse directly.

- Wellbeing challenges and events: Team competitions, challenges, and events that drive engagement.

Why choose Espresa: The value here is breadth. If your goal is total rewards, and the lifestyle spending account is one piece of a program that also includes recognition and wellbeing, consolidating onto one platform beats stitching point tools together. It fits people teams that treat engagement as a core metric, not a byproduct.

Espresa pricing: Espresa does not publicly list pricing on its site. On G2, Espresa holds a 4.2/5 rating.

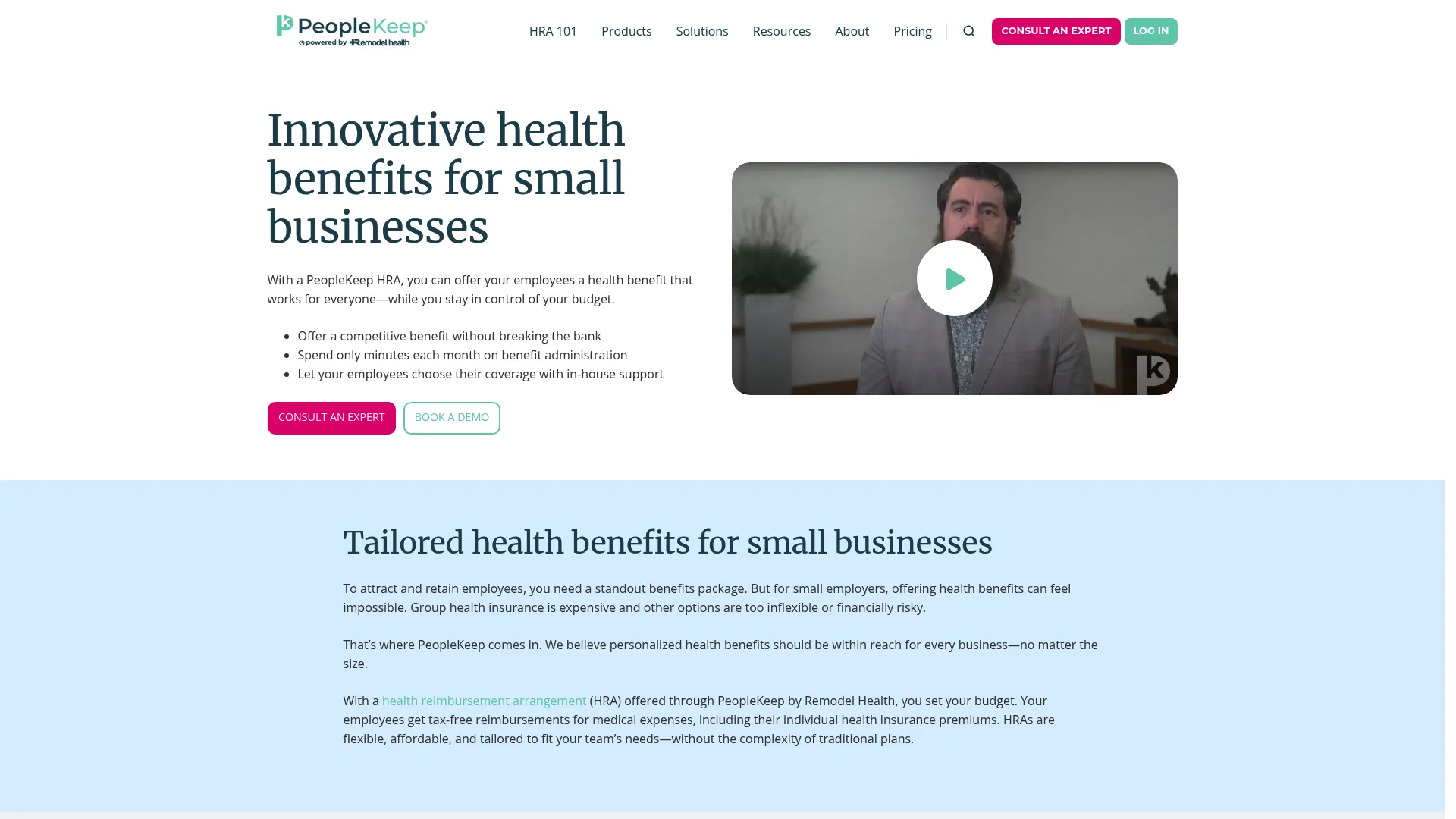

4. PeopleKeep

PeopleKeep is HRA administration software for employers offering personalized health benefits, with a strong claims review and reimbursement workflow. While its center of gravity is health reimbursement arrangements rather than pure lifestyle accounts, it earns a spot for teams that want broader benefits administration software with clear tax and compliance framing.

Best for: Small and midsize employers needing HRA administration alongside reimbursement workflows.

Key strengths

- QSEHRA, ICHRA, and GCHRA administration: Structured support for the main HRA types.

- Claims review and reimbursement workflow: Substantiation and reimbursement handled inside the tool.

- Integrated shopping: Employees select coverage through built-in shopping.

Why choose PeopleKeep: If your reimbursement needs lean toward health benefits and you value education-first compliance content, PeopleKeep is transparent about tax treatment and how each arrangement works. It fits smaller employers who want a documented, predictable reimbursement workflow rather than a broad lifestyle marketplace.

PeopleKeep pricing: PeopleKeep's public pricing page lists QSEHRA at $25/employee/month, ICHRA starting at $25/employee/month, and GCHRA at $12/employee/month, with base fees and a three-seat minimum. On G2, PeopleKeep holds a 4.4/5 rating.

5. WEX

WEX is a global B2B fintech platform spanning fleet cards, business payments, and employee benefits administration. It belongs on an enterprise shortlist when an LSA is one line item inside a much larger benefits and payments relationship. If you are already evaluating WEX for adjacent products, folding lifestyle accounts into the same infrastructure can simplify vendor management.

Best for: Larger businesses needing fleet, payments, or benefits infrastructure at scale.

Key strengths

- Benefits administration: Employer benefits handled within a broad platform.

- Business payments: Payment processing and disbursement infrastructure.

- Enterprise scale: Built for organizations running multiple benefit and payment programs.

Why choose WEX: The case for WEX is consolidation at scale. If your organization already runs payments or fleet products through it, adding benefits administration keeps procurement and integrations in one relationship. Verify LSA-specific workflow depth during evaluation, since the platform spans far beyond lifestyle accounts.

WEX pricing: WEX does not publish general public pricing; product pages route to contact and RFP flows, and the visible fee pages are region-specific schedules. A verified G2 rating was not available at publication.

6. Fringe

Fringe is an employee experience platform covering rewards, recognition, wellbeing, gifting, swag, and lifestyle benefits through a marketplace model. Employees choose from a curated catalog rather than submitting receipts, which makes it the marketplace-first pick on this list. It ranks here for teams that want engagement and curated choice bundled together.

Best for: HR teams wanting to consolidate recognition, perks, wellbeing, and gifting into one platform.

Key strengths

- Rewards and recognition: Recognition programs alongside lifestyle benefits.

- Lifestyle benefits and stipends: Marketplace-driven lifestyle spending and stipends.

- Wellbeing offerings: Challenges and wellbeing content that lift participation.

Why choose Fringe: The marketplace model trades the receipt workflow for curated choice, which many employees find more engaging than a reimbursement form. If you want to consolidate several perk and recognition tools into one employee experience, Fringe is designed for that. It also has the clearest public pricing on this list.

Fringe pricing: Fringe publishes per-employee-per-month pricing. Growth runs $3/PEPM for teams under 1,000 employees, Scale runs $2/PEPM for 1,000 to 10,000, and Enterprise is custom for organizations above 10,000. There is no free tier. On G2, Fringe holds a 4.7/5 rating.

7. ThrivePass

ThrivePass is an employee benefits platform that pairs a Lifestyle Spending Account, branded the Thrive Account, with pre-tax accounts like FSA, HSA, HRA, and commuter, plus rewards and recognition. That combination makes it worth a look for employers who want lifestyle and pre-tax accounts administered together under one vendor.

Best for: Mid-sized to enterprise employers wanting unified benefits administration and reimbursement.

Key strengths

- Lifestyle Spending Account: The Thrive Account for employer-funded lifestyle benefits.

- Pre-tax accounts: FSA, HSA, HRA, and commuter administration in one place.

- Rewards and recognition: Engagement layered onto the benefits stack.

Why choose ThrivePass: If you run both pre-tax accounts and a lifestyle account, one vendor for both reduces integration and reconciliation overhead. It suits mid-market and enterprise teams that want reimbursement and pre-tax administration consolidated. Confirm LSA reporting and eligibility depth against your policy during evaluation.

ThrivePass pricing: ThrivePass does not display public pricing on its own site, using demo-request CTAs. A third-party Capterra listing shows a starting price of $0.55 flat per month. The company displays a 4.1/5 G2 badge on its homepage.

8. Joon

Joon is a lifestyle spending account platform for employer-funded benefits and automated reimbursements. It is reimbursement-first and built to be simple: customizable allowances, cadences, and eligibility rules, with automated reimbursement of eligible purchases. For smaller teams or a straightforward benefit program, it is the fastest to stand up.

Best for: Employers wanting a flexible, automated lifestyle spending account without heavy setup.

Key strengths

- Automated reimbursement: Eligible purchases reimbursed automatically.

- Customizable rules: Allowances, cadences, and eligibility rules set to your policy.

- HRIS and SSO integrations: Connections and international coverage built in.

Why choose Joon: When you want a clean reimbursement-first LSA without a lengthy implementation, Joon's simplicity is the draw. Transparent flat pricing makes it easy for a finance team to model, and the customizable allowances cover most single-program needs. It fits teams launching their first LSA who value speed and predictability.

Joon pricing: Joon publishes pricing starting at $250/month for a Base plan, which includes one allowance and cadence, unlimited eligible categories, a dedicated account manager, and live chat support. There is no free tier. A verified G2 rating was not available at publication.

9. BenefitHelp Solutions

BenefitHelp Solutions is an employee benefits administration and reimbursement account services provider, covering FSA, HRA, COBRA, and retiree administration. It rounds out the list as an outsourced-administration option, best suited to employers and brokers who want reimbursement account services handled by a partner rather than a self-serve platform.

Best for: Employers and brokers needing outsourced benefits administration and reimbursement account services.

Key strengths

- Flexible Spending Accounts: FSA administration with card and reimbursement methods.

- Health Reimbursement Arrangements: HRA administration and claims processing.

- COBRA and retiree administration: Broader account services under one provider.

Why choose BenefitHelp Solutions: If your need is practical, outsourced reimbursement account administration rather than a modern self-serve LSA product, BenefitHelp Solutions fits. Its member-facing portal and reimbursement options cover the operational basics. Evaluate it on software fit and reporting depth if a dedicated lifestyle account is your primary goal.

BenefitHelp Solutions pricing: BenefitHelp Solutions does not publicly display pricing; the site directs visitors to request a quote. A verified G2 rating was not available at publication.

Considerations before you buy

Before you sign, run every finalist through this checklist.

Operating model fit

Decide reimbursement-first, card-based, or marketplace before comparing features. The model shapes admin effort, employee experience, and how substantiation works. Reimbursement-first gives the most control; card-based gives the most immediacy; marketplace gives the most curated choice.

Tax treatment and compliance

Confirm the platform treats LSA funds as taxable income and pushes the taxable amount to payroll automatically. Ask how it handles substantiation requirements and keeps an audit trail. Weak compliance handling moves the work back to your finance team.

Payroll and HRIS integration

Verify native connections to your payroll and HRIS, or at minimum a clean export. Because most LSA reimbursements are taxable, an accurate payroll feed is not optional. A broken integration turns every pay cycle into manual reconciliation.

Reporting and reimbursement speed

Check that finance can pull spend by category, utilization, and taxable totals on demand. Then test reimbursement speed with a real claim during evaluation. Slow payouts quietly erode the participation that makes the benefit worth offering.

LSA software pricing model

Understand whether pricing is per employee, flat, or quote-based, and what scales with headcount. Model the cost at your projected size. A per-employee rate that looks small can grow fast as you hire.

Conclusion

The right lifestyle spending account software depends on your operating model more than any single feature. If control, clean substantiation, and taxable-income handling matter most, a vendor-agnostic reimbursement-first platform like Compt is the safest default, with Joon a strong pick for smaller teams that want speed. If employee experience and immediacy lead, a card-based option like Benepass fits. If engagement and curated choice matter, a marketplace model like Fringe or a total rewards platform like Espresa makes sense. For broader benefits administration, PeopleKeep, ThrivePass, WEX, and BenefitHelp Solutions each cover adjacent account types.

Your next step: shortlist two finalists that match your operating model, then test each against reimbursement speed, compliance and payroll integration, and the actual admin effort of a live claim. That comparison, not the feature grid, tells you which platform earns its place in your stack.

If you also run go-to-market motions and want to see how teams present products interactively, explore Guideflow and its interactive demo format, or browse related roundups like the best employee advocacy software tools.

FAQs

Lifestyle spending account software is a benefits administration platform that lets employers fund and manage flexible, employer-funded lifestyle and wellness benefits. It automates eligibility rules, receipt substantiation, reimbursement or card spending, tax treatment, and reporting, so a program that once lived in a spreadsheet runs on its own.

In almost all cases, yes. LSA funds are treated as taxable income to the employee, which is why these programs run as post-tax reimbursements. Good lsa software pushes the taxable amount into payroll automatically so it is reported correctly without manual reconciliation.

An FSA and HSA are pre-tax accounts governed by strict IRS rules on eligible medical expenses. An lsa account is employer-funded, post-tax, and far more flexible, letting the employer define its own eligible categories, from fitness to childcare to home office gear. The flexibility comes at the cost of the tax advantage.

Yes. In a reimbursement-first model, employees pay out of pocket, submit a receipt through the platform, and get reimbursed through payroll or direct deposit. The software captures the receipt, checks it against eligibility rules, and routes the taxable amount to payroll.

Because there is no fixed IRS list, the employer decides. Common categories include fitness and gym memberships, wellness and mental health, childcare and family support, home office equipment, professional development, and travel. The software enforces whatever eligibility rules you set.

Most platforms let you define eligible expense categories, set allowance amounts per employee group, and configure cadences without a support ticket. The tool then enforces those rules automatically at claim or card-spend time and captures substantiation for the audit trail.

Neither is universally better; it depends on your priority. Card-based LSA spending is more immediate and often feels better to employees, with merchant category controls enforcing eligibility. Reimbursement-first gives more control, cleaner substantiation, and simpler taxable-income handling. Many platforms support both.

Confirm automated taxable-income handling and a clean payroll feed, native payroll and HRIS integration, on-demand reporting for spend and taxable totals, and real reimbursement speed tested on a live claim. Then model the LSA software pricing at your projected headcount to avoid cost surprises as you scale.