Your loan officers rekey borrower data three times before a file reaches underwriting. Documents live in email threads. Compliance checks happen at the end, when a missed disclosure means restarting the clock. Every one of those handoffs adds days to your time-to-close and cost to your per-loan economics.

That friction is not a people problem. It is a systems problem. And it compounds as volume grows.

The market is telling lenders the same thing. The mortgage servicing software market reached roughly $6.03B in 2026 and is projected to hit $8.2B by 2030, according to Research and Markets (2026). More than 65% of lenders in developed regions now run digital mortgage platforms for loan origination, per Congruence Market Insights (2025). The teams that standardize their workflow are the ones protecting margin while the Mortgage Bankers Association forecasts around $2.2T in single-family origination volume for 2026.

Choosing the right mortgage software is the difference between a repeatable lending operation and a stack of manual handoffs that only works when your best processor is at their desk. This guide compares eight mortgage software companies across the full lending lifecycle so you can shortlist the two or three that fit your channel, your team size, and your compliance reality. If you evaluate software the way you'd evaluate any growth system, you'll recognize the same buyer discipline covered in guides like our best marketing automation software tools roundup.

What's inside

This guide is for mortgage brokers, retail lenders, community banks, credit unions, and independent mortgage banks (IMBs) evaluating mortgage lending software in 2026. Some of you are replacing a legacy loan origination system. Others are buying a first real platform to move off spreadsheets.

We selected the eight tools based on four criteria that matter for operational leverage:

- Workflow automation depth across application intake, document collection, and underwriting handoffs

- Compliance support, including audit trails and disclosure management

- Integration maturity with CRMs, pricing engines, AUS, and core banking systems

- Borrower experience and fit by business model, from solo brokers to enterprise lenders

The list spans point-of-sale (POS), full LOS platforms, and all-in-one lending systems, so you can compare across the stack, not just within one category.

TL;DR

- Best for all-in-one lending operations: MeridianLink, for institutions running consumer and mortgage lending on one platform

- Best for digital borrower experience: Floify, for lenders and brokers who want a configurable POS front end

- Best for enterprise-grade LOS depth: Encompass, for process-heavy, highly regulated operations

- Best for smaller teams or broker workflows: Calyx Point, for brokers who want a proven LOS with borrower intake add-ons

- Best for integration-heavy organizations: OpenClose, for lenders modernizing legacy workflows with omnichannel origination

- Best for lean lending teams: LendingWise, for private and commercial lenders or brokers needing end-to-end operations without heavy setup

What is mortgage software?

Mortgage software is the category of systems that lenders use to originate, process, underwrite, close, and service home loans. It replaces manual, document-heavy workflows with structured automation, compliance controls, and a shared record every stakeholder can see.

Most buyers evaluate three overlapping layers. A point-of-sale (POS) system handles the borrower-facing front end: the application, document upload, status transparency, and eSign. A loan origination system (mortgage LOS) runs the internal engine: processing, underwriting workflow, conditions, disclosures, and closing. Borrower portals give applicants a self-serve window into their loan. An all-in-one lending platform combines several of these layers, sometimes across consumer and mortgage products in a single system.

Understanding where each tool sits in that stack is the first filter. A broker replacing a paper intake process needs different software than a bank consolidating consumer and mortgage lending onto one platform.

Core capabilities to expect from modern mortgage software systems:

- Application intake with a borrower-friendly digital experience

- Document collection and management with automated requests and tracking

- Underwriting workflow with conditions, tasks, and role-based routing

- Compliance controls for disclosures, audit trails, and regulatory checks

- Closing support, including eSign and clear-to-close coordination

- Integrations with pricing engines, AUS, CRMs, and core systems via API integrations

- Reporting and analytics for pipeline visibility and pull-through

The strongest digital mortgage platforms tie these together so a file moves from application to clear-to-close without leaving the system.

When to use mortgage software

Replace manual workflows

Spreadsheets, shared inboxes, and ad hoc checklists work until they don't. They break the moment two people touch the same file or volume spikes. There's no single source of truth, no audit trail, and no way to see where a loan is stuck. Mortgage software replaces that with structured workflow automation, so a file follows the same path every time and nothing depends on one person's memory.

Standardize borrower intake

Inconsistent intake creates rework downstream. A borrower who uploads the wrong document, or none at all, becomes a processor's problem three days later. Mortgage software unifies the application and documentation flow into one guided experience. The borrower sees exactly what's needed, uploads it once, and your team pulls it into the same place every time. That consistency is what makes the borrower experience feel professional and your operation feel repeatable.

Reduce cycle time and compliance risk

Every manual handoff is a chance to lose days and introduce compliance exposure. Automation and audit trails let teams move faster with less rework, and they create the documentation you need when an examiner asks how a decision was made. Shorter time-to-close and cleaner compliance are not competing goals. The same system delivers both.

Comparison table

Pricing and G2 ratings shift often, so verify current figures on each vendor's site and G2 listing before you commit. The table below reflects values confirmed at publication.

| # | Product | Intent | Key differentiation | Pricing | G2 rating |

|---|---|---|---|---|---|

| 1 | Floify | Digital POS and automation | Configurable borrower portal and document workflows | Lender and Broker editions; quote-based | 4.8/5 |

| 2 | MeridianLink | All-in-one lending platform | Consumer plus mortgage lending on one system | Quote-based | 4.1/5 |

| 3 | Encompass | Enterprise LOS | End-to-end origination and workflow automation | Contact sales | 4.3/5 |

| 4 | Calyx Point | Broker-friendly LOS | Traditional LOS with borrower intake add-on | ZIP add-on from $3/application | 3.8/5 |

| 5 | Mortgage Builder | Residential LOS | Retail, wholesale, and correspondent production | Quote-based | Not listed |

| 6 | OpenClose | Integration-heavy LOS | Omnichannel origination, now part of MeridianLink | Quote-based | 2.8/5 |

| 7 | BytePro | LOS workflow support | Lender operational workflow tooling | Quote-based | Not listed |

| 8 | LendingWise | Lean lending operations | LOS, CRM, and servicing for private lenders | From $119/mo | Not listed |

The 8 best mortgage software tools for 2026

1. Floify

Floify is a digital mortgage point-of-sale and automation platform built for lenders and brokers who want a configurable front end without rebuilding their whole stack. It sits at the borrower-facing layer, handling the application, document collection, and loan status transparency, then feeds that data cleanly into your LOS. If your biggest friction is intake and document chase, this is where Floify earns its place.

Best for: Mortgage lenders and brokers who need a configurable digital loan origination workflow layered on top of an existing LOS.

Key strengths

- Borrower portal and document collection: A branded application and document portal that automates requests and tracks what's outstanding.

- Configurable workflows and branding: Customize the intake flow and apply your brand so the borrower experience feels like yours, not a vendor's.

- Native eSign and integrations: Built-in eSign plus connections to LOS platforms, CRMs, pricing engines, and AUS.

Why choose Floify: Choose Floify when the borrower-facing experience is your competitive edge and you want to keep your existing LOS. It's the layer that removes document friction and gives applicants real-time loan progress transparency. Solo brokers and mid-sized lenders both use it because the workflow configuration scales without forcing a full platform migration.

Floify pricing: Floify publicly offers a Lender Edition with a per-loan pricing option and a Broker Edition, but no numeric public price was visible on its site at publication. Request a quote for your channel and volume. Floify holds a 4.8/5 rating on G2, the highest on this list.

2. MeridianLink

MeridianLink is a digital lending platform for financial institutions that covers account opening, consumer lending, mortgage lending, collections, and analytics in one system. For a community bank or credit union running multiple lending lines, the appeal is consolidation: one platform, one data model, fewer integrations to maintain. That operational simplification is exactly what a founder-minded operator looks for when reducing tools while increasing signal.

Best for: Community banks, credit unions, and IMBs needing an integrated digital lending platform across consumer and mortgage products.

Key strengths

- Account opening and digital applications: Unified digital application workflows across product lines, not just mortgage.

- Consumer and mortgage origination: Run both motions on one platform instead of stitching separate systems together.

- Collections and reporting analytics: Built-in analytics give leadership pipeline and portfolio visibility without exporting to spreadsheets.

Why choose MeridianLink: Choose MeridianLink when your institution originates more than mortgages and wants one platform to run consumer and mortgage lending together. The modular architecture means you adopt what you need now and expand later. It fits operationally complex lenders who value a single data model over a collection of best-of-breed point tools.

MeridianLink pricing: MeridianLink uses quote-based pricing; no public numeric price was visible on its site at publication. Pricing scales with institution size and modules. It holds a 4.1/5 seller rating on G2.

3. Encompass

Encompass, from ICE Mortgage Technology, is a mortgage loan origination platform that connects and streamlines the full lending workflow. It's the deep, end-to-end LOS most enterprise buyers benchmark against. Encompass covers origination, integrated sales tools, mortgage loan pricing, and digital processing through closing, all inside one system built for scale and regulatory rigor.

Best for: Mortgage lenders needing a single system for loan origination and workflow automation across a high-volume, highly regulated operation.

Key strengths

- Loan origination workflow automation: Structured automation across the origination lifecycle to reduce manual handoffs.

- Integrated sales tools and pricing: Mortgage loan pricing and sales tooling built into the origination flow.

- End-to-end digital processing and closing: Digital mortgage processing that carries a file from application through closing.

Why choose Encompass: Choose Encompass when you run a process-heavy, compliance-intensive operation and need a mortgage LOS that covers the entire lifecycle in one connected system. Enterprise lenders evaluate it for the depth of its workflow automation and its established ecosystem. If your priority is breadth and rigor over lightweight setup, this is the benchmark.

Encompass pricing: Encompass does not publish public pricing; its materials direct buyers to contact sales for a quote. Expect enterprise packaging aligned to volume and modules. It holds a 4.3/5 rating on G2.

4. Calyx Point

Calyx Point is a mortgage loan origination system for brokers, bankers, and financial institutions. It's a long-established LOS that brokers know well, covering the loan lifecycle from application to closing with an optional borrower point-of-sale add-on called ZIP. For a smaller broker shop that wants a proven, practical LOS without enterprise overhead, Point remains a common default.

Best for: Mortgage brokers needing a traditional mortgage broker software LOS with borrower intake add-ons.

Key strengths

- End-to-end loan origination: Covers the workflow from application through closing in one familiar interface.

- Borrower point-of-sale add-on (ZIP): Optional borrower intake layer that adds a digital front end when you need it.

- Broad integration network: Connections with 200+ vendor partners for pricing, AUS, and services.

Why choose Calyx Point: Choose Calyx Point when you're a broker or small lender who wants a configurable, widely adopted LOS with a shallow learning curve for teams already familiar with it. The ZIP add-on lets you bolt on borrower-facing intake only when it pays off. It fits teams that value practicality and adoption over platform breadth.

Calyx Point pricing: Public standalone pricing for the core Point LOS was not visible at publication. The ZIP point-of-sale add-on is priced from $3 per loan application, with an eSign package at $1.50 per transaction, and requires a Point subscription. Calyx Point holds a 3.8/5 rating on G2.

5. Mortgage Builder

Mortgage Builder, now part of Constellation Mortgage Solutions, is a residential loan origination system for mortgage lenders. It covers end-to-end residential origination and supports retail, wholesale, and correspondent production, with an open-architecture database and workflow customization. For lenders running multiple production channels who want focused LOS functionality, it's worth a look.

Best for: Mortgage bankers, banks, and credit unions needing enterprise loan origination software across multiple production channels.

Key strengths

- End-to-end residential origination: Handles the residential loan lifecycle inside one system.

- Multi-channel production support: Retail, wholesale, and correspondent workflows in one platform.

- Open-architecture customization: An open database and configurable workflows for lenders with specific process needs.

Why choose Mortgage Builder: Choose Mortgage Builder when you produce across retail, wholesale, and correspondent channels and want a single LOS to manage them. The open architecture appeals to teams that need to tailor workflows rather than accept defaults. Honest fit note: this is a focused LOS for lenders who want origination depth over an all-in-one consumer lending suite.

Mortgage Builder pricing: Mortgage Builder uses quote-based pricing; no public numeric price was visible on its site at publication. Contact the vendor for packaging aligned to your channels and volume.

6. OpenClose

OpenClose, now part of MeridianLink, is mortgage lending software focused on digital loan origination and borrower experiences. It's a cloud-based mortgage LOS with an omnichannel digital mortgage experience and built-in pricing and document automation. For mid-market lenders modernizing legacy workflows, OpenClose sits at the intersection of origination depth and integration flexibility.

Best for: Banks, credit unions, and mortgage lenders needing enterprise mortgage LOS software with strong integration flexibility.

Key strengths

- Cloud-based loan origination: A modern, cloud-native LOS built to replace on-premise legacy systems.

- Omnichannel digital experience: Consistent borrower and lender workflows across channels.

- Built-in pricing and document automation: Pricing and document workflows automated inside the platform.

Why choose OpenClose: Choose OpenClose when you're a mid-market lender modernizing off a legacy mortgage lender software stack and want a cloud LOS with flexible integrations. Its place within MeridianLink means it connects into a broader lending ecosystem. Plan implementation as a project with clear milestones, as you would with any platform replacement that touches your core workflow.

OpenClose pricing: OpenClose uses quote-based pricing; no public numeric price was visible on its site at publication. Pricing is aligned to institution size and deployment scope. It holds a 2.8/5 rating on G2, so weigh recent reviews against your specific requirements during evaluation.

7. BytePro

BytePro is loan origination software positioned around lender operational efficiency and workflow support. It's aimed at lenders who want a focused mortgage LOS to run processing and origination workflows. For teams that value a dedicated origination system over a sprawling all-in-one suite, it's a candidate for the shortlist.

Best for: Mortgage lenders who prefer a focused LOS built around origination workflow and operational efficiency.

Key strengths

- Origination workflow support: Structured workflows for processing and moving files through the pipeline.

- Operational efficiency focus: Built to reduce manual steps in day-to-day lending operations.

- Lender-oriented tooling: Functionality aimed at lender teams managing origination at volume.

Why choose BytePro: Choose BytePro when you want a dedicated loan origination system focused on operational throughput rather than a broad consumer lending platform. It suits lenders who prefer depth in origination over breadth across products. As with any LOS decision, run a structured evaluation against your actual workflow bottlenecks before committing.

BytePro pricing: Public numeric pricing for BytePro's mortgage LOS was not confirmed from a first-party source at publication. Contact the vendor directly for packaging and a quote aligned to your operation.

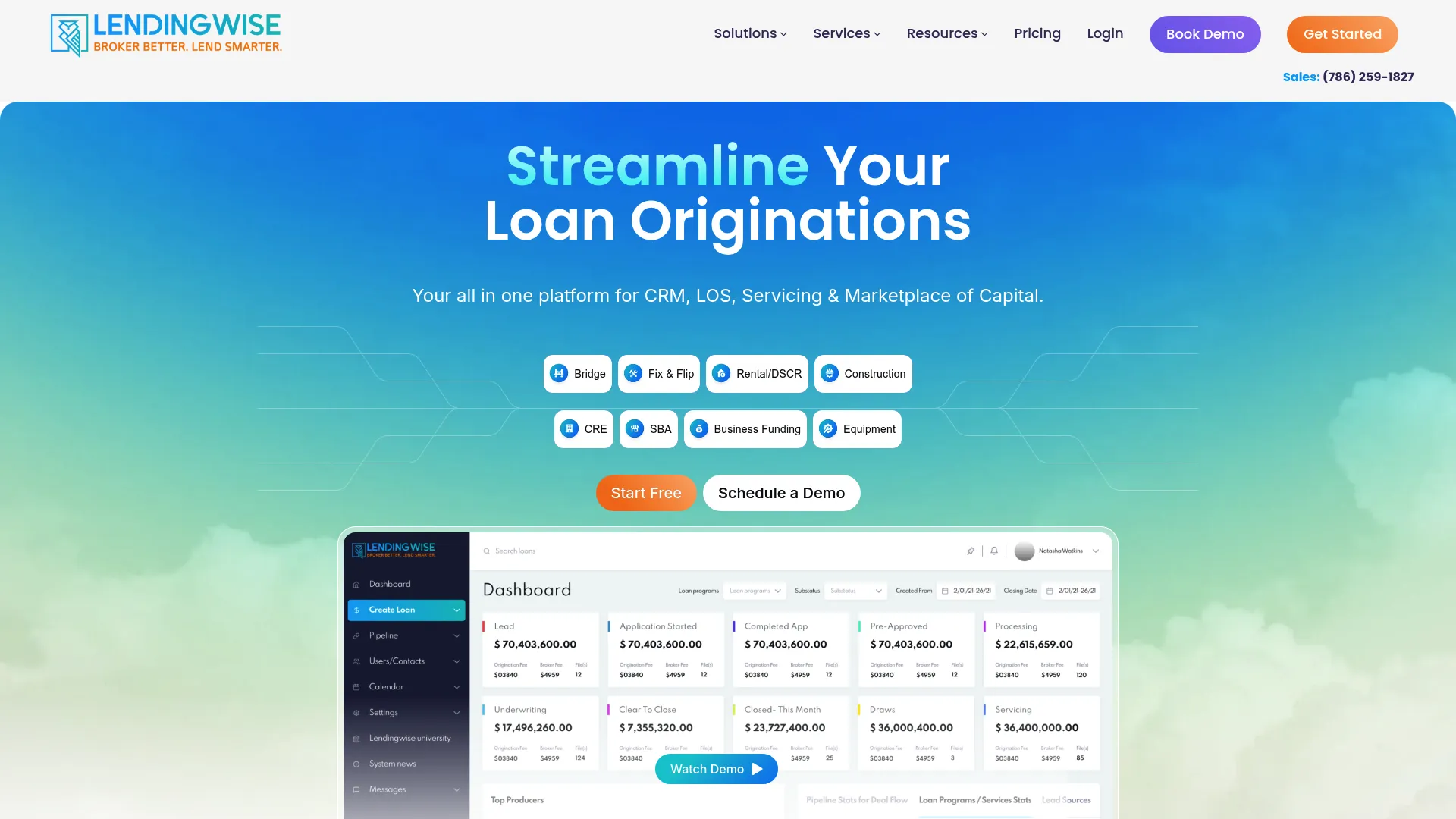

8. LendingWise

LendingWise is an all-in-one loan origination, CRM, servicing, and marketplace platform for private and commercial lenders and brokers. It combines lead pipeline, origination, processing, servicing, and borrower and broker portals in one place, with white-labeling and marketplace options. For a lean team that wants accessible mortgage software without heavy setup, it's one of the more approachable entry points on this list.

Best for: Private and commercial lenders or brokers needing an end-to-end lending operations platform without enterprise overhead.

Key strengths

- CRM and pipeline management: Lead and pipeline tools built into the same system as origination.

- Origination, processing, and servicing: End-to-end workflows plus draw management for construction and rehab loans.

- Portals and white-labeling: Borrower, broker, and loan officer portals with white-label and marketplace options.

Why choose LendingWise: Choose LendingWise when you're a lean private or commercial lending team that wants CRM, origination, and servicing in one accessible platform. The tiered plans and ease-of-use make it a practical first real system for smaller operations. It fits teams that want to move fast without a long implementation cycle.

LendingWise pricing: LendingWise publishes tiered pricing starting at $119/mo for a Starter plan, $600/mo for Pro, and $1,595/mo for Elite, with a custom Enterprise tier. Pricing details vary slightly across its own pages, so confirm current tiers and any discount billing before you buy. Capterra reviewers rate it favorably; no G2 rating was confirmed at publication.

Considerations before you buy

Shortlisting is where most of the value is. Before you sign anything, pressure-test each finalist against the criteria that actually move your per-loan economics.

Channel and business model fit

A solo broker and a multi-channel IMB have almost nothing in common operationally. Match the platform to your production model: retail, wholesale, correspondent, or a mix. Buying enterprise LOS depth you don't need is as costly as outgrowing a lightweight tool in a year.

Compliance and audit depth

Compliance is not a feature you bolt on later. Ask how each system handles disclosures, timing, and audit trails. You want documentation an examiner can follow and controls that catch a missed step before it becomes a violation, not after.

Integration and API maturity

Your mortgage software has to talk to your pricing engine, AUS, CRM, and core banking system. Ask for the specific integrations you rely on today, and ask about API integrations for the ones you'll need next. A platform that forces manual rekeying between systems reintroduces the friction you're trying to remove.

Implementation burden and time-to-value

The best platform is worthless if it takes nine months to go live. Ask for a realistic implementation timeline, what your team has to provide, and when you'll originate the first live loan. Weigh setup effort against the ROI you expect in the first two quarters.

Total cost against volume

Per-loan, per-seat, and flat-rate models behave very differently as you scale. Model the cost at your current volume and at 2x. The cheapest entry tier can become the most expensive option once your pipeline grows.

Conclusion

There's no single best mortgage software, only the best fit for your channel, team size, compliance needs, and integration maturity. For all-in-one lending across consumer and mortgage lines, MeridianLink leads. If the borrower experience is your edge, Floify layers a configurable POS onto your existing stack. For enterprise-grade LOS depth in a regulated operation, Encompass sets the benchmark. Brokers and smaller lenders should look hard at Calyx Point, while OpenClose fits integration-heavy modernization and LendingWise gives lean teams an accessible all-in-one.

Don't try to compare all eight at once. Pick the two or three that match your business model, then test each against your real workflow bottlenecks: where files stall, where compliance risk hides, and where your team rekeys data. The right loan origination system removes those bottlenecks and gives you a repeatable operation, not just new software.

Shortlist, run a focused evaluation, and choose the system that earns its place in your stack within the first quarter.

Start your journey with Guideflow today!

FAQs

Mortgage software is the set of systems lenders use to originate, process, underwrite, close, and service home loans. It replaces manual, document-heavy workflows with structured automation, compliance controls, and a shared record every stakeholder can access. Categories include point-of-sale front ends, loan origination systems, borrower portals, and all-in-one lending platforms.

Mortgage software is the broad category; a loan origination system (mortgage LOS) is one part of it. The LOS runs the internal engine, processing, underwriting workflow, conditions, disclosures, and closing, while a point-of-sale system handles the borrower-facing application and document collection. Many all-in-one platforms combine both layers, plus servicing and CRM.

Prioritize workflow automation across intake and underwriting, compliance controls with audit trails, and API integrations with your pricing engine, AUS, CRM, and core systems. Borrower experience and reporting depth follow close behind. The right weighting depends on where files stall in your current process.

Brokers often favor Calyx Point for a proven, familiar LOS with an optional borrower intake add-on, and Floify for a configurable digital POS front end. LendingWise is a strong fit for private and commercial lending brokers who want CRM, origination, and servicing in one accessible platform. Match the choice to your loan types and volume.

Banks and credit unions running consumer and mortgage lending together tend to evaluate MeridianLink for its single-platform approach and OpenClose for cloud-based origination with strong integration flexibility. Institutions with high-volume, highly regulated mortgage operations often benchmark Encompass for its end-to-end LOS depth.

Pricing models vary widely. LendingWise publishes tiers starting at $119/mo, while Calyx Point's ZIP point-of-sale add-on starts at $3 per loan application. Enterprise platforms like Encompass, MeridianLink, Mortgage Builder, and OpenClose use quote-based pricing tied to institution size, volume, and modules. Model cost at current and projected volume before committing.

For compliance-heavy teams, audit depth is a primary selection criterion, not an afterthought. Ask how each system manages disclosure timing, documents every decision, and produces records an examiner can follow. A platform that automates compliance checks earlier in the workflow reduces both rework and regulatory exposure.

Ask about the specific systems you depend on today: pricing engines, automated underwriting systems, your CRM, document services, and core banking. Confirm whether connections are native or require middleware, and ask about API integrations for future needs. Manual rekeying between disconnected tools reintroduces the exact friction mortgage software is meant to remove.