Your users already pay for something inside your product. A subscription, a marketplace transaction, a vendor payout. Right now most of that money probably leaves your app to settle somewhere else. Every redirect is a drop-off point, a support ticket, and revenue you watch flow past you.

The temptation is to build payments yourself. Then you read the fine print: PCI scope, KYC/AML onboarding, fraud prevention, settlement timing, dispute handling. Suddenly you are staffing a payments operation instead of shipping your roadmap. That is the tension every product team hits when they evaluate embedded payments software.

The numbers explain why teams keep reaching for it anyway. Global embedded payment transaction value is projected to grow from $1.1 trillion in 2024 to $2.5 trillion by 2028, a 134% jump, according to Juniper Research (2024). Bain & Company (2021) put U.S. B2B embedded payments revenue on a path from $1.9 billion to $6.7 billion by 2026. The money is moving inside software, not around it.

This guide compares the best embedded payments software for SaaS and platform businesses in 2026. The goal is not to crown one winner. It is to help you match a provider to your motion, whether you want a faster launch, deeper control over money movement, or bank-backed trust for regulated buyers. If your evaluation work overlaps with adjacent stack decisions, our roundups of the best customer data platform and the best AI cybersecurity solutions cover neighboring buying criteria.

What's inside

This is a comparison of eight embedded payments platforms built to put payments inside your app, your workflows, and your customer journeys instead of bouncing users to a third-party checkout. It is written for Product Managers running a build-versus-buy decision, not for payments specialists who already live in the rails.

We selected and ranked tools on five criteria that matter to a software team:

- API quality and developer experience: how clean the integration is and how much engineering it demands.

- Monetization fit: whether the model lets you turn payments into a revenue line.

- Compliance support: how much PCI, KYC/AML, and risk scope the provider absorbs.

- Enterprise readiness: security, trust signals, and the ability to scale.

- Use-case fit: vertical SaaS, marketplaces, regulated sectors, or broad horizontal platforms.

TL;DR

Short on time? Here are the decision shortcuts for embedded payment solutions in 2026:

- Best for breadth and developer experience: Stripe covers the widest range of payment capabilities through one API.

- Best for payments plus banking: Unit pairs money movement with accounts, cards, and adjacent embedded finance products.

- Best for vertical SaaS payfac: Rainforest Pay handles compliance scope so platforms can monetize without building payments operations.

- Best for platform payouts: WePay (backed by JPMorgan Chase) supports marketplace and platform payment flows.

- Best for payment economics control: Finix gives software platforms processing control and clear unit economics.

- Best for white-label launch speed: Unipaas packages branded, configurable embedded payments for SaaS.

- Best for regulated sectors: Dream Payments fits banks, insurers, and compliance-heavy software.

- Best for bank-backed trust: Newline by Fifth Third combines payments and deposit APIs under a bank charter.

What are embedded payments?

Embedded payments are payment capabilities built directly into a software product so users pay without leaving the host experience. Instead of redirecting to an external gateway, the platform owns the checkout, the flow, and often the money movement that follows.

Embedded payments sit inside the broader category of embedded finance, which also covers banking, lending, cards, and insurance delivered through non-financial software. Payments are usually the first piece a platform embeds because the demand is already there: customers are transacting whether or not the platform participates.

Under the hood, most embedded payment solutions share the same moving parts:

- Payment APIs: the developer interface that lets your app create charges, manage payouts, and move money programmatically.

- Tokenization: replacing card data with a non-sensitive token so your platform avoids holding raw card numbers.

- Authorization and settlement: the authorization confirms funds are available; settlement is when money actually lands.

- Payment rails: the underlying networks (card networks, ACH, wires, instant payments) that carry the funds.

- Risk controls: KYC/AML onboarding, fraud prevention, and dispute or chargeback handling.

A quick note on language. Integrated payments and embedded payments get used interchangeably, but they are not the same. Integrated payments usually bolt a third-party processor onto an existing flow, where the payment still feels like a separate step. Embedded payments make the transaction feel native to your product, with the platform controlling the experience and, often, a share of the economics. For a Product Manager, that difference shows up directly in activation, checkout UX, and how much revenue the platform can capture.

When to use embedded payments software

Embedded payments are not a default add-on. They earn their place when the product surface, the business model, or the customer experience makes native money movement the obvious move.

Launch payments inside an existing SaaS workflow

When your product already owns user attention at the moment money changes hands, embedding payments removes a context switch. A field service tool that lets a technician collect payment on-site, or an invoicing app that completes the transaction in-app, keeps the user inside one flow. Fewer redirects mean fewer drop-offs and a shorter path to first value.

Monetize a platform or marketplace

For platforms and marketplaces, payments are not just a feature. They become a revenue line. When you facilitate transactions between buyers and sellers, embedded payments let you take a share of volume, set attach rates, and turn a cost center into platform revenue. This is where embedded payments for platforms shifts from UX nicety to business model.

Reduce checkout drop-off and support burden

Every external redirect is a chance for the user to abandon, get confused, or open a ticket. Keeping payments in-app reduces handoffs, improves conversion, and cuts the "where did my payment go" support load. For teams measuring activation and retention, that handoff reduction often shows up faster than the revenue does.

Comparison table

The table below summarizes the eight providers on intent, primary use case, pricing, and rating. Pricing models vary widely across embedded payments, so treat these as starting points and confirm current terms with each vendor.

| # | Product | Intent | Key use case | Pricing | G2 rating |

|---|---|---|---|---|---|

| 1 | Stripe | Broad payments infrastructure | Developer-first online payments and platform payments | 2.9% + 30¢ per successful charge | 4.4/5 |

| 2 | Unit | Embedded finance + payments | Banking, payments, cards, and capital for platforms | Contact sales | 3.5/5 |

| 3 | Rainforest Pay | Payfac-as-a-service | Vertical SaaS payments monetization | From 0.30% + $0.30 | Not listed |

| 4 | WePay | Platform payments | Marketplace and SaaS payouts | 2.9% + 25¢ per transaction | 3.6/5 |

| 5 | Finix | Payments infrastructure | Processing control and platform economics | From $250/month | Not listed |

| 6 | Unipaas | White-label embedded payments | Branded, configurable SaaS checkout | Custom quote | Not listed |

| 7 | Dream Payments | Embedded pay-in and payout | Banks, insurers, regulated software | Interchange plus 1.8% | Not listed |

| 8 | Newline by Fifth Third | Bank-backed embedded finance | Enterprise payments and deposit APIs | Contact sales | Not listed |

1. Stripe

Stripe is the financial infrastructure platform most teams benchmark everything else against. It handles payments processing, billing and subscriptions, and a deep set of fraud prevention and payment tooling through APIs that engineers genuinely like working with. For embedded payments, Stripe Connect lets platforms onboard sub-merchants, route payouts, and take a share of volume, which makes it a serious option for SaaS and marketplace monetization.

The reason Stripe shows up first is breadth. Most embedded payment solutions specialize. Stripe spans online payments, in-app payments, recurring billing, and adjacent financial products, so a product team rarely outgrows the core platform.

Best for: software teams that want developer-friendly online payments plus room to expand into adjacent financial infrastructure.

Key strengths

- Developer experience: clean, well-documented payment APIs that shorten integration time and reduce engineering drag.

- Capability breadth: payments, subscriptions, fraud tooling, and platform payments in one stack.

- Ecosystem depth: extensive integrations, libraries, and documentation that lower the cost of maintenance over time.

Why choose Stripe: If you want the broadest, most documented payments infrastructure and a low risk of hitting a capability wall, Stripe is the safe default. It fits teams that value engineering velocity and want optionality as the product grows, rather than a narrowly packaged vertical solution.

Stripe pricing: Stripe's standard payments pricing starts at 2.9% + 30¢ per successful charge. Custom pricing is available for larger or specialized volume, and adjacent products carry their own pricing. There is no free tier, though there is no upfront cost to start integrating. Stripe holds a 4.4/5 rating on G2.

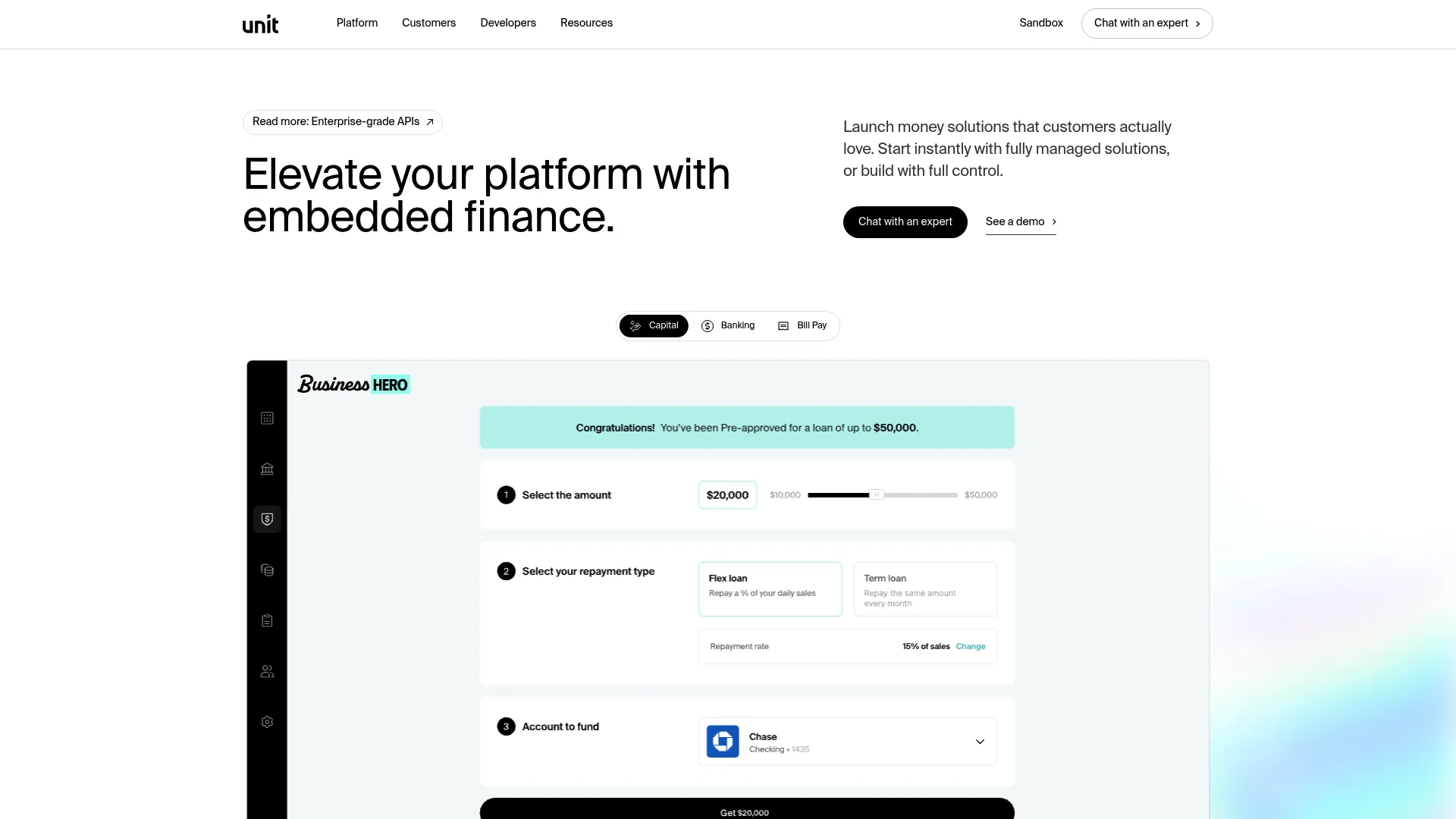

2. Unit

Unit is an embedded finance platform that lets software companies offer banking, payments, cards, and capital. Where most providers stop at moving money, Unit gives platforms accounts and wallets with real routing and account numbers, money movement across ACH, wires, checks, and bill pay, plus card issuing with API/SDKs and white-label UI components.

That scope is the point. If your roadmap goes beyond accepting payments toward holding balances, issuing cards, or offering capital, Unit lets you build that without becoming a chartered institution yourself.

Best for: fintech and B2B software platforms that want embedded banking and payments infrastructure in one place.

Key strengths

- Money movement depth: ACH, wires, checks, and bill pay through a single integration.

- Accounts and wallets: FBO accounts with real routing and account numbers for genuine balance holding.

- Card issuing: API-first card programs with white-label UI components.

Why choose Unit: Choose Unit when payments are one part of a larger embedded finance ambition. Teams that want to layer accounts, cards, and capital onto their product get a more complete platform than a payments-only provider can offer. It fits product teams thinking in terms of a financial product line, not a single checkout feature.

Unit pricing: Unit does not publish pricing. The company directs prospects to contact sales for pricing and order minimums, which is typical for embedded finance platforms with custom risk and compliance scope. Unit holds a 3.5/5 rating on G2, based on a small number of reviews.

3. Rainforest Pay

Rainforest Pay is an embedded payments and payfac software platform built specifically for software companies that want to embed and monetize payments. It offers white-labeled, embeddable onboarding, payments, reporting, and chargeback management, and supports card, ACH, Apple Pay, and card-present transactions. Webhook automation, stored payments, and Plaid validation round out the developer surface.

Its angle is payfac-as-a-service. Rainforest absorbs much of the compliance scope a platform would otherwise own, so vertical SaaS teams can add payments without standing up a full payments operation.

Best for: vertical SaaS platforms that want to embed and monetize payments without building deep payments operations.

Key strengths

- Payfac-as-a-service: reduces the compliance and operational burden of becoming a payment facilitator.

- White-label components: embeddable onboarding, payments, reporting, and chargeback management under your brand.

- Broad acceptance: card, ACH, Apple Pay, and card-present support from one integration.

Why choose Rainforest Pay: Pick Rainforest when you want platform revenue from payments but do not want to own the payments compliance stack. Its no-revenue-share buy-rate pricing and developer-friendly components fit growing vertical SaaS companies that care about unit economics and time-to-launch in equal measure.

Rainforest Pay pricing: Rainforest uses interchange-plus buy-rate pricing with tiered card volume and per-item fees, starting around 0.30% + $0.30 per card transaction, with ACH at $0.20 per item and no revenue share. A verified G2 rating was not available at publication.

4. WePay

WePay is integrated payments infrastructure for software platforms and ISVs, backed by JPMorgan Chase. It focuses on merchant onboarding, payment processing, and withdrawals to bank accounts, which makes it a fit for marketplaces, crowdfunding platforms, and SaaS products that need to move money to many recipients.

The Chase backing is a meaningful trust signal for platforms that want bank-grade stability behind their embedded payments without negotiating a bank partnership directly.

Best for: software platforms that need embedded payments plus payout workflows to multiple parties.

Key strengths

- Platform payouts: built-in merchant onboarding and withdrawals for marketplace and platform models.

- Bank backing: JPMorgan Chase infrastructure behind the payments layer.

- Integration simplicity: designed to embed payments into platform products without heavy custom build.

Why choose WePay: WePay fits platforms whose core need is collecting payments and distributing funds to sellers, hosts, or recipients. If marketplace-style money movement and a recognizable banking partner matter more than the broadest API surface, WePay is a strong candidate for embedded payments for platforms.

WePay pricing: WePay's publicly listed standard pricing for new U.S. businesses is 2.9% + 25¢ per transaction, with ACH potentially carrying a different rate. There is no free tier. WePay holds a 3.6/5 rating on G2.

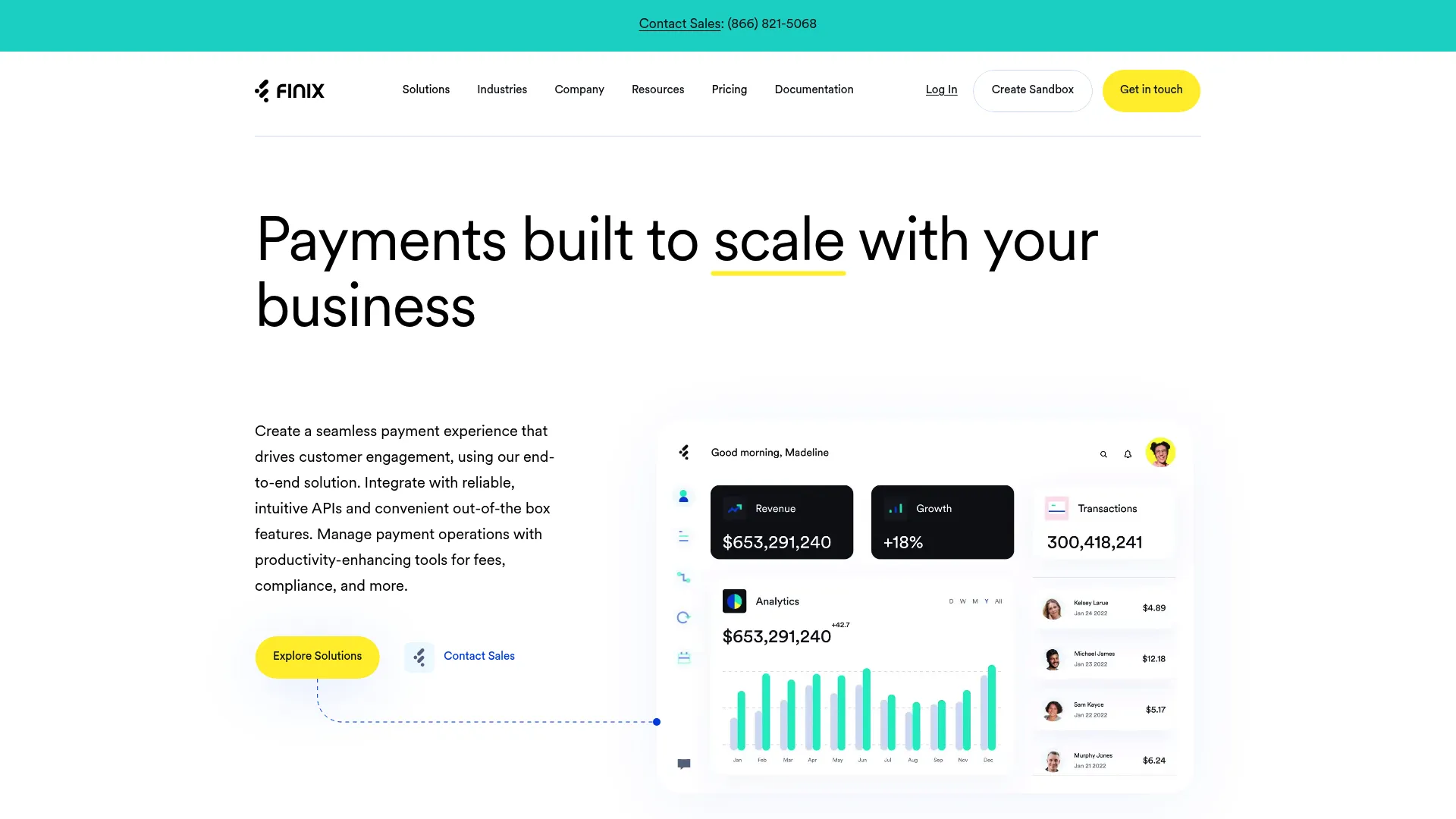

5. Finix

Finix is a payments infrastructure platform for software platforms, marketplaces, and direct merchants. It provides embedded payments and payment APIs, merchant onboarding, payouts, and compliance tools, plus no-code and low-code checkout, a virtual terminal, and fraud and dispute tooling. The pitch centers on giving software companies control over payment processing and the economics behind it.

For platforms that process meaningful volume, owning more of the payments stack can change the unit economics. Finix is built for teams that want that control rather than handing the full margin to a third party.

Best for: businesses building embedded payments or managing merchant payment operations at scale.

Key strengths

- Processing control: more ownership of the payments stack and the economics that come with it.

- Flexible integration: no-code, low-code, and full-API checkout options for different team capacities.

- Operational tooling: merchant onboarding, payouts, compliance, and fraud and dispute management.

Why choose Finix: Finix suits platforms with enough volume to benefit from better payment economics and a team willing to own more of the stack. If you have moved past "just make payments work" and into "make payments profitable," its architecture and pricing model reward that scale.

Finix pricing: Finix's public pricing for direct merchants starts at $250 monthly on its Standard plan, which includes 0% markup on interchange and card network fees, with additional transaction fees listed. Custom pricing is available for larger or specialized needs. There is no free tier. A meaningful G2 rating was not available at publication.

6. Unipaas

Unipaas is an embedded payments platform for SaaS and digital platforms that want to embed and manage payments under their own brand. It offers white-label embedded payments components, managed payments operations and compliance support, and a payments product set spanning checkout, invoice, subscription, pay-by-link, capital, and payment terminals.

The packaging is the differentiator. Unipaas leans toward a configurable, branded experience that lets a SaaS team launch payments quickly without assembling each piece from scratch.

Best for: SaaS platforms that want to embed and manage branded payments with a packaged, configurable approach.

Key strengths

- White-label components: branded checkout and payment surfaces that match your product.

- Managed operations: payments operations and compliance support handled by the provider.

- Broad product set: checkout, invoice, subscription, pay-by-link, capital, and terminals from one platform.

Why choose Unipaas: Unipaas fits teams that value a packaged, brand-controlled payments experience and a faster path to launch. If you want configurable components and managed compliance rather than a from-scratch build, it lands well for SaaS platforms prioritizing time-to-market and brand consistency.

Unipaas pricing: Unipaas uses bespoke, quote-based pricing. The pricing page asks prospects to submit a form for a personalized quote, which fits its configurable, platform-specific model. A verified G2 rating was not available at publication.

7. Dream Payments

Dream Payments is an embedded payments and payout platform for banks, insurers, and software platforms. It provides embedded pay-in and payout APIs, hosted and embedded checkout, and a range of payout methods including virtual cards, bank transfers, Interac e-Transfer, and cheque payouts. The emphasis on regulated sectors makes it distinct from more horizontal providers.

For teams selling into banking, insurance, or other compliance-heavy verticals, the trust and regulatory posture matters as much as the API. Dream Payments is positioned for exactly those buyers.

Best for: banks, insurers, and software platforms that need embedded payment and payout workflows in regulated contexts.

Key strengths

- In-context payments: embedded pay-in and payout APIs that keep transactions inside the host experience.

- Flexible payouts: virtual cards, bank transfers, Interac e-Transfer, and cheque options.

- Regulated-sector fit: built with the compliance posture banks and insurers expect.

Why choose Dream Payments: Choose Dream Payments when your buyers operate in regulated environments and trust signals carry weight. Its payout breadth and API-based implementation suit financial and insurance software that needs to move money in and out reliably under scrutiny.

Dream Payments pricing: Dream Payments describes an interchange-plus model with a 1.8% markup, though a full public plan table was not visible at publication. A verified G2 rating was not available.

8. Newline by Fifth Third

Newline by Fifth Third is an API-first embedded finance platform for enterprise payment, card, and deposit solutions, backed directly by Fifth Third Bank. It offers ACH, wire, book transfer, and instant payments APIs, virtual and physical card issuing, and FDIC-insured bank accounts with virtual reference numbers. The bank charter behind it is the headline.

That bank-backed model matters for enterprises that need deposit capabilities alongside payments and want a regulated institution in the stack rather than a layer on top of one.

Best for: enterprises building embedded payments and deposit products with a direct bank partner.

Key strengths

- Bank-backed trust: direct Fifth Third Bank charter behind payments and deposits.

- Payments plus deposits: ACH, wire, instant payments, and FDIC-insured accounts in one platform.

- Card issuing: virtual and physical card programs through an API-first model.

Why choose Newline by Fifth Third: Newline fits enterprise teams where bank-grade trust and deposit capabilities are non-negotiable. When your use case requires both payments and held balances under a regulated charter, a bank-linked model removes a layer of counterparty risk that platform-only providers cannot.

Newline pricing: Newline does not publish pricing publicly; engagement runs through its sales and partnership process, consistent with enterprise, bank-backed embedded finance. A verified G2 rating was not available at publication.

Considerations before you choose

Positive fit is only half the decision. Before you commit, run the shortlist through a buyer's checklist built for a Product Manager's reality.

Compliance scope

Know exactly how much the provider absorbs. PCI scope, KYC/AML onboarding, and fraud prevention can sit with the platform, the provider, or be shared. Payfac-as-a-service models typically take on more of the compliance burden, while infrastructure providers may leave more with you. Get the boundary in writing.

Developer effort

Estimate the real integration cost, not the marketing version. Clean payment APIs, SDKs, and webhook support shorten the build, but no-code and low-code components can compress timelines further. Weigh this against your engineering opportunity cost, since every sprint on payments is a sprint off your roadmap.

Monetization model

Decide how payments earn. Some providers support revenue share and attach rates that turn payments into platform revenue; others optimize for low cost rather than margin. If monetization is the goal, confirm the model supports it before integration, not after.

Support and implementation

Look at onboarding, documentation, and how the provider handles disputes and edge cases. The difference between a smooth launch and a stalled one is often support quality, especially for teams without payments expertise in-house.

Enterprise readiness and trust

For regulated or enterprise buyers, the provider's trust posture is part of your product. Bank backing, FDIC-insured accounts, and security certifications can shorten your customers' procurement reviews. Match the provider's enterprise readiness to the buyers you actually sell to.

Conclusion

There is no single best embedded payments platform, only the best fit for your motion. Stripe wins on breadth and developer experience. Unit goes deepest when payments are one piece of a larger embedded finance plan. Rainforest Pay and Unipaas suit vertical SaaS teams that want monetization and speed without owning compliance. Finix rewards platforms with the volume to benefit from payment economics control. WePay covers marketplace payouts with bank backing, while Dream Payments and Newline by Fifth Third bring regulated-sector and bank-grade trust.

The right next step is narrow, not broad. Shortlist two or three providers that match your build-versus-buy stance, then pressure-test each on compliance scope, integration effort, and monetization model with your own engineering and finance stakeholders. Embedded payments are product design and revenue strategy at once, so treat the choice as a roadmap decision, not just a checkout feature. Decide what you want most, speed, control, breadth, or regulated trust, and let that anchor the shortlist.

FAQs

Embedded payments software lets a platform offer payments inside its own product instead of redirecting users to an external processor. The platform owns the checkout, the experience, and often a share of the transaction economics. It is how SaaS and platform businesses make money movement feel native rather than bolted on.

Integrated payments usually attach a third-party processor to an existing flow, so the payment still feels like a separate step. Embedded payments make the transaction feel native to the product, with the platform controlling the experience and, often, the monetization. The practical difference shows up in checkout UX, conversion, and how much revenue the platform captures.

Prioritize API quality and developer experience, compliance support across PCI and KYC/AML, monetization options like revenue share and attach rates, clear reporting, and the speed your team can realistically ship. Match the provider's enterprise readiness to the buyers you sell to. The best choice depends on whether you optimize for speed, control, or breadth.

Platforms typically earn through transaction fees, volume-based revenue, and attach rates on payments they facilitate. Beyond direct revenue, embedded payments improve retention by keeping users inside the product and reducing reasons to churn. For many platforms, payments shift from a cost center to a meaningful platform revenue line.

PCI scope, KYC/AML onboarding, fraud prevention, and tokenization are the core concerns. Tokenization keeps raw card data off your systems, while KYC/AML governs who you can onboard. For regulated or enterprise buyers, trust signals like bank backing and FDIC-insured accounts also factor into their own procurement reviews.

It varies by provider, integration depth, and compliance requirements. Packaged, white-label, and no-code or low-code options often launch faster, while deeper infrastructure builds that give you more control take longer. Estimate the engineering opportunity cost honestly, since payments work competes with your product roadmap.

The case weakens when payment frequency is low, margins are thin, or the compliance burden outweighs the upside. If users rarely transact inside your product, or if the revenue from payments would not cover the integration and maintenance cost, a lighter integrated payment approach may be the better call.

Payments are one part of embedded finance, the broader category that also includes banking, lending, cards, and insurance delivered through non-financial software. A platform might start with embedded payments and later expand into accounts, cards, or capital. Embedded finance is the full menu; embedded payments are usually the first dish software companies serve.