You spent 45 minutes updating a client's retirement projection last night. Then their spouse asked one "what if we retire two years earlier" question in the meeting, and you were back in the software rebuilding assumptions while everyone watched the cursor spin.

That is the real problem with most advisory workflows. Not that the planning math is hard. It's that the tools slow down the moment a client wants to see something specific, and every plan update becomes a manual project instead of a repeatable process. If you run a firm, that friction compounds. Every advisor rebuilds plans their own way, plan presentation quality varies by who built it, and nothing scales without you in the room.

The category has grown up around exactly this pain. The global financial planning software market was estimated at $5.82B in 2025 and is forecast to reach $25.06B by 2035, a 15.72% CAGR according to Precedence Research (2025). North America alone accounted for roughly 38 to 39% of that market in 2025. That growth reflects a shift in what advisors expect from financial planning software: not just a Monte Carlo engine, but client collaboration, scenario modeling, and a workflow that holds up under real-time questions.

If you are evaluating financial advisor tools as an operator, the question is not which platform has the most features. It's which one produces repeatable plans, clean client collaboration, and plan presentation your whole team can deliver without you. This guide compares the platforms that do that best. For teams thinking about how they show any product experience to clients, the same principle behind an interactive demo applies here: show, don't tell.

What's inside

This is a shortlist of five financial advisor software platforms for 2026, evaluated for advisory firms and RIAs choosing planning software, not portfolio management systems or generic budgeting apps. We selected based on four criteria that matter to operators: planning depth (retirement, tax, cash flow, and scenario modeling), client collaboration and client portal quality, plan presentation and visual outputs, and workflow repeatability at scale. We also weighted credibility signals like G2 ratings and public pricing transparency. Each entry covers who it fits, what it does well, and what it costs where that data is public.

TL;DR

- Best overall for deep planning workflows: eMoney Advisor, for firms that need comprehensive planning depth plus a strong client-facing experience.

- Best for visual planning and client collaboration: RightCapital, for advisors who want approachable client communication with serious planning under the hood.

- Best for transparent pricing and clear plan delivery: Moneytree, for advisors who value published pricing and presentation clarity.

- Best for broad ecosystem and established workflows: Envestnet | MoneyGuide, for firms that want a widely adopted goal-based planning platform.

- Best free resource hub: Investor.gov, for calculators, retirement tools, and research at zero cost.

The right pick depends on your dominant workflow. Match the tool to the planning job you run most, not the longest feature list.

What is financial advisor software?

Financial advisor software is a category of financial planning software for advisors that helps them model client scenarios, build and present financial plans, collaborate with clients between meetings, and standardize planning workflows across a firm. It sits at the center of the advisor tech stack, connecting the planning engine to a client communication layer and an operational system.

These platforms do more than run projections. They turn raw client data into plans clients understand, then keep those plans current as life changes.

Core capabilities across the category include:

- Retirement planning: Project income, spending, and longevity, usually with Monte Carlo analysis to stress-test outcomes.

- Scenario modeling: Show the impact of retiring earlier, selling a business, or changing savings rates in real time.

- Tax planning: Model Roth conversions, tax-efficient withdrawals, and multi-year tax strategies.

- Cash flow planning: Track income and expenses year by year across a client's full timeline.

- Client portal: Give clients a secure place to view plans, upload documents, and track progress between meetings.

- Plan presentation: Produce visual outputs like net worth charts, blueprints, and summaries that make complex plans legible.

- Shared access and collaboration: Let advisors and clients work from the same plan, so updates do not require a full rebuild.

Think of the category as three layers stacked together. A planning engine does the math. A client collaboration layer keeps clients engaged. And an operational system standardizes how every advisor in the firm builds and delivers plans. The best financial planning software does all three without forcing you to pick.

When to use financial advisor software

Show planning outcomes clients can act on

Use it when clients need to see the consequences of a decision, not just hear about them. Retirement planning software that runs a live scenario, showing how retiring two years early changes the Monte Carlo success rate, turns an abstract tradeoff into a concrete choice. The same applies to tax planning and cash flow planning: the value is in making the numbers visible.

Keep client collaboration alive between meetings

Use it when the relationship depends on more than annual reviews. A modern client portal lets clients check progress, upload documents, and revisit their plan on their own time. That client collaboration keeps the plan current and reduces the "where do we stand" emails that pile up between meetings.

Standardize planning as your firm scales

Use it when you are adding advisors and can no longer personally review every plan. Repeatable plan creation, standardized plan presentation, and shared templates mean a new hire builds plans the same way your best advisor does. For a founder or firm owner, that repeatability is the difference between a workflow that scales and one that routes through you. The same logic that drives teams to build repeatable onboarding flow systems applies to plan delivery.

Comparison table

Here is how the five platforms compare on intent, primary use case, pricing, and G2 rating. Pricing reflects publicly listed figures as of mid-2026; where a vendor does not publish prices, the field notes that.

| # | Product | Intent | Key use case | Pricing | G2 rating |

|---|---|---|---|---|---|

| 1 | eMoney Advisor | Comprehensive planning + client engagement | Deep planning with account aggregation and a client portal | Not publicly listed; varies by organization | 4.7/5 |

| 2 | RightCapital | Visual planning + client collaboration | Retirement, tax, and insurance planning with a client-friendly portal | From $149.95 per advisor/month | 4.6/5 |

| 3 | Moneytree | Transparent planning + clear delivery | Goals-based and cash-flow planning with published pricing | From $1,195 per user/year | 4.1/5 |

| 4 | Envestnet | MoneyGuide | Established goal-based planning | Goal-based plans, estate strategies, and client presentations | From $3,000 per advisor annually |

| 5 | Investor.gov | Free public tools | Calculators, retirement tools, and fraud research | Free | Not rated |

The table is a starting filter. The sections below explain the workflow each platform fits, so you can match the tool to how your firm actually plans.

1. eMoney Advisor

eMoney Advisor is financial planning software built for advisors and firms that need scalable planning depth alongside a strong client-facing experience. It pairs goals-based and cash flow planning with account aggregation, reporting, and a client portal, which makes it a fit for firms that want the full picture of a client's financial life in one place. If your practice leans on comprehensive plans and ongoing client engagement, eMoney is built for that combination.

Where eMoney stands out is the connection between planning depth and client experience. Account aggregation pulls a client's held-away assets into the plan, so retirement planning and cash flow planning reflect reality rather than what the client remembered to mention. The client portal and mobile app keep clients looking at their plan between meetings, which is where client collaboration actually happens. For scenario modeling, advisors can walk through changes and show clients the downstream effect on their long-term outlook.

Best for: Firms that need comprehensive planning depth plus an engaging client-facing experience at scale.

Key strengths

- Account aggregation: Pulls held-away accounts into the plan so projections reflect a client's complete financial picture.

- Client portal and mobile app: Keeps clients engaged with their plan between meetings, strengthening client collaboration.

- Planning breadth: Combines goals-based and cash flow planning with reporting and integrations across the advisor tech stack.

Why choose eMoney Advisor: Choose eMoney when your firm's value is the depth and thoroughness of the plan, and when client engagement between meetings matters as much as the plan itself. It fits established RIAs and larger practices that want one system covering planning, aggregation, and client communication rather than stitching those layers together.

eMoney Advisor pricing: eMoney does not publish subscription prices. The company states pricing varies based on the needs of the organization and directs advisors to contact sales or start a free trial. Product tiers are named Plus, Pro, and Premier, with capabilities scaling up across them. Because there is no public price, budget-conscious buyers should request a quote early in evaluation. On G2, eMoney holds a 4.7/5 rating.

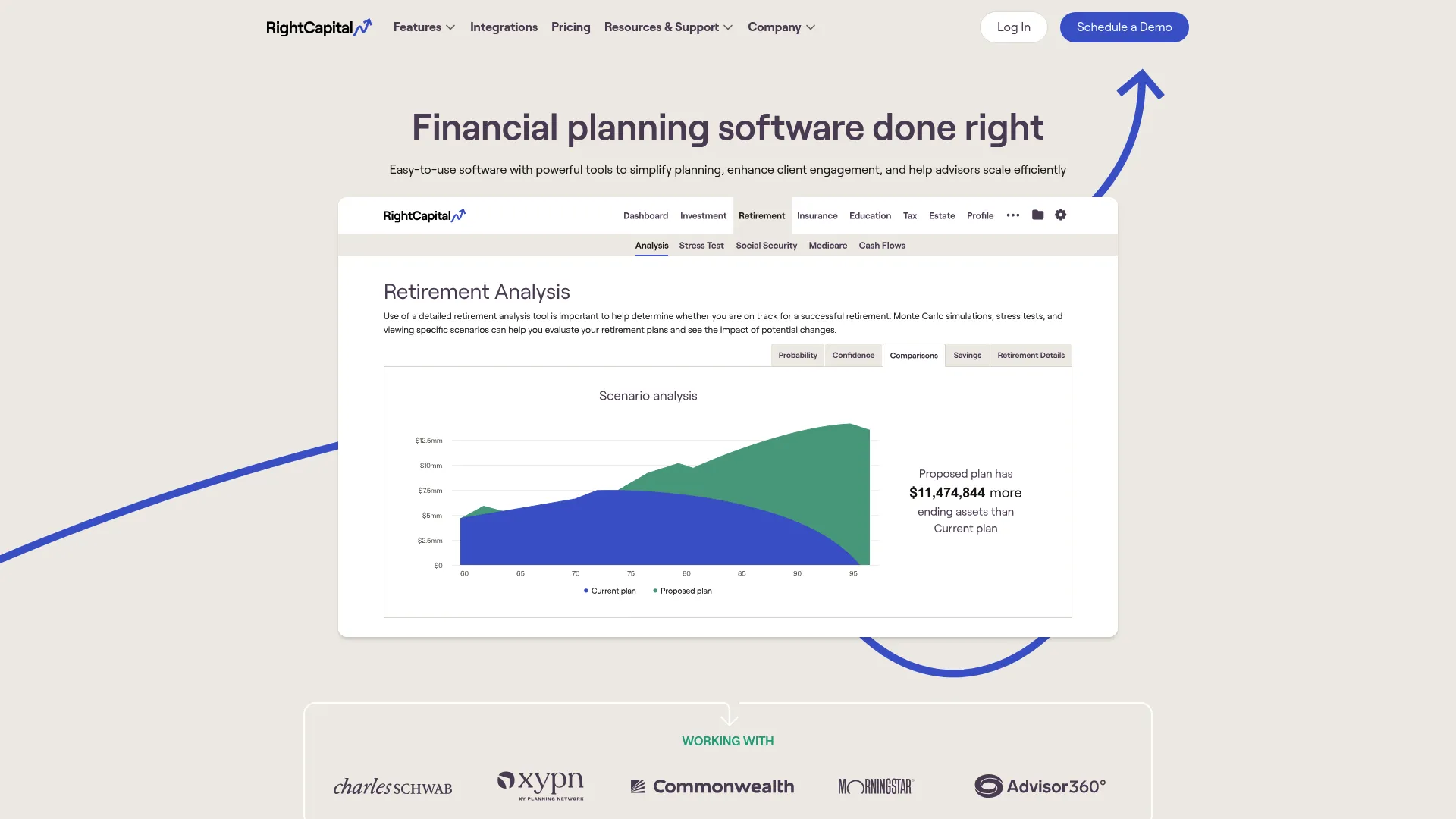

2. RightCapital

RightCapital is financial planning software for advisors and RIAs that balances serious planning capability with client-friendly presentation. It covers retirement planning, tax planning, investment analysis, insurance needs review, and risk assessment, then wraps the output in visual tools like Snapshot, Blueprint, and the Cash Flow Map. For advisors who want planning depth without overwhelming clients, RightCapital hits that balance well.

The visual layer is the differentiator. RightCapital's retirement planning software runs Monte Carlo scenario analysis, but the client sees a clean Snapshot rather than a wall of numbers. Its tax planning module models Roth conversions and tax-efficient withdrawal strategies, which matters for advisors who compete on tax alpha. The advisor client portal and mobile app handle tasks, document sharing, and plan access, so client collaboration continues between meetings. That combination of depth and legibility is why RightCapital has grown fast among independent advisors.

Best for: Advisors and RIAs who want strong planning capability paired with approachable, client-friendly communication.

Key strengths

- Retirement and scenario modeling: Runs Monte Carlo analysis and presents outcomes clients can actually read.

- Tax planning: Models Roth conversions and tax-efficient withdrawals for advisors who compete on tax strategy.

- Visual client portal: Delivers Snapshot, Blueprint, and Cash Flow Map through an advisor client portal that keeps clients engaged.

Why choose RightCapital: Choose RightCapital when client communication is central to how you win and keep clients, and when you want tax and retirement depth without a steep client learning curve. It fits growing independent RIAs that need modern client collaboration and clean plan presentation at a transparent price.

RightCapital pricing: RightCapital publishes its pricing. Plans start with Basic at $149.95 per advisor per month, Premium at $209.95, and Platinum at $254.95, with an Enterprise tier available through sales. A 14-day free trial is available, and the first year requires an annual commitment. That transparency makes RightCapital easy to budget against, a real advantage when comparing RIA software. On G2, RightCapital holds a 4.6/5 rating.

3. Moneytree

Moneytree is financial planning software for advisors built around transparent assumptions and clear plan delivery. It supports both goals-based planning and cash-flow-based planning, and pairs those with a client portal and secure document sharing. Advisors who value showing clients exactly how a projection was built, rather than hiding it behind a black-box engine, tend to gravitate toward Moneytree.

The core appeal is trust through transparency. Moneytree lets advisors expose the assumptions behind a plan, which supports honest client conversations about retirement planning and long-term cash flow planning. Its visual delivery makes projections legible, and secure document sharing through the client portal keeps client collaboration organized. Moneytree also publishes its pricing openly, which is a useful signal for firms comparing total cost across the advisor tech stack. For advisors who want a planning workflow they can explain line by line, that clarity is the draw.

Best for: Advisors who want transparent, explainable planning with published pricing and clean presentation.

Key strengths

- Transparent assumptions: Exposes the inputs behind a plan so advisors can walk clients through the reasoning.

- Goals and cash-flow planning: Supports both goals-based and detailed cash flow planning in one workflow.

- Client portal: Provides secure document sharing and plan access to keep client collaboration organized.

Why choose Moneytree: Choose Moneytree when transparency and explainability are core to your advice philosophy, and when you prefer knowing your software cost upfront. It suits independent advisors and smaller firms that want a scalable planning workflow without opaque enterprise pricing.

Moneytree pricing: Moneytree publishes its pricing clearly. The Essential plan, which covers goals-based planning, starts at $1,195 per user per year. The Elite plan adds cash-flow planning and advanced capabilities at $2,195 per user per year. An Enterprise tier is available through sales. There is no free tier. That published, per-year model makes Moneytree straightforward to compare against monthly-billed RIA software. On G2, Moneytree Advise holds a 4.1/5 rating.

4. Envestnet | MoneyGuide

Envestnet | MoneyGuide is advisor-focused financial planning software for building and presenting client plans, with deep roots in goal-based planning. It's one of the most widely adopted planning platforms among advisors, which means broad familiarity across the industry and a large base of advisors already trained on it. The platform covers advanced estate strategies, detailed cash-flow planning, and dynamic net worth over time, positioning it as an established engine for firms that want a proven workflow.

MoneyGuide's strength is its goal-based planning approach and its place in a broad ecosystem. The modular workflow, including MyBlocks for targeted planning conversations, lets advisors run focused sessions on a single topic rather than always building a full plan. Its living plan positioning encourages advisors to keep plans current, supporting ongoing client collaboration rather than one-and-done planning. For scenario modeling around retirement and estate questions, MoneyGuide's engine is well-established. Firms that value industry familiarity and integration breadth often land here.

Best for: Firms that want an established, widely adopted goal-based planning platform with broad advisor familiarity.

Key strengths

- Goal-based planning: A mature engine built around client goals, retirement projections, and net worth over time.

- Modular MyBlocks workflow: Lets advisors run focused planning conversations on a single topic without building a full plan.

- Estate and cash-flow depth: Supports advanced estate strategies and detailed cash-flow planning for complex client situations.

Why choose Envestnet | MoneyGuide: Choose MoneyGuide when broad adoption and industry familiarity matter, and when you want a platform that many advisors already know how to use. It fits firms that value an established planning engine and want the option to plug into a wider Envestnet ecosystem.

Envestnet | MoneyGuide pricing: MoneyGuide publishes a list price for its main subscription: $3,000.00 per advisor on an annual subscription, with a monthly-paid option. Add-on integrations like Yodlee through the client portal and MX with MoneyGuide run $400.00 annually per user each. There is no free tier. Advisors should confirm which capabilities are bundled versus add-on before comparing total cost. On G2, Envestnet | MoneyGuide holds a 4.0/5 rating.

5. Investor.gov

Investor.gov is the SEC's investor education site, offering free tools, guides, alerts, and fraud-prevention resources for individual investors. It is not a commercial planning platform and does not build or store client plans. It earns a place on this shortlist as the zero-cost baseline: a trustworthy source of calculators and research that advisors and clients can lean on without a subscription.

The value is in credibility and utility. Investor.gov hosts free financial planning tools and calculators, including retirement and compound-interest calculators, plus access to EDGAR filings and adviser background checks. For an advisor, it is a useful supplement, a place to point clients for unbiased education, verify a professional's registration, or run a quick calculation. It will not replace dedicated financial advisor software for plan creation, scenario modeling, or a full client portal, but it complements a paid platform as a research and trust-building resource. Treat it as the low-cost floor when you compare the category.

Best for: Advisors and clients who want free, SEC-backed calculators, research, and fraud-prevention resources.

Key strengths

- Free calculators and tools: Retirement and compound-interest calculators available at no cost.

- Fraud and background research: Alerts, bulletins, and adviser background checks backed by the SEC.

- Education library: Neutral investor education articles advisors can share with clients.

Why choose Investor.gov: Choose Investor.gov as a free supplement, not a core planning system. It is the right resource when you want unbiased calculators, want to verify a registration, or need a credible source to point clients toward for self-education.

Investor.gov pricing: Investor.gov is free. It is a government-operated resource with no subscription tiers or pricing page, because it is publicly funded. There is no G2 rating, which is expected for a public utility rather than a commercial product.

Considerations before you buy

Before committing to any financial planning software, run each option through the criteria that actually predict fit for your firm.

Planning depth versus client legibility

The best plan is worthless if the client cannot follow it. Evaluate whether the platform's scenario modeling and Monte Carlo analysis produce outputs a client understands in a meeting. Depth and legibility are both required; weigh how each tool balances them against how your clients think.

Client portal and collaboration quality

A client portal is now table stakes, but quality varies widely. Test how easily clients log in, view plans, upload documents, and revisit their plan on mobile. Strong client collaboration between meetings drives retention, so treat the portal as a core feature, not an add-on.

Workflow repeatability across your team

If you are scaling, the question is whether every advisor can build and present plans the same way. Look for templates, standardized plan presentation, and shared access that make plan creation repeatable. This is what lets a firm grow without routing every plan through the founder.

Total cost and pricing transparency

Compare published pricing where it exists, and request quotes early where it does not. Per-advisor monthly pricing and per-user annual pricing are not directly comparable, so normalize to an annual per-seat figure. Factor add-ons, aggregation fees, and integration costs into total cost of ownership across your advisor tech stack.

Integration with your existing stack

Planning software rarely lives alone. Confirm it connects cleanly to your CRM, custodian, and any wealth management software you run. Fragmented data creates manual work, which is the exact friction good software should remove.

Conclusion

The five platforms here solve different jobs. eMoney Advisor fits firms that need comprehensive planning depth with strong client engagement. RightCapital fits advisors who want visual, client-friendly planning with real tax and retirement capability. Moneytree fits advisors who value transparency and published pricing. Envestnet | MoneyGuide fits firms that want an established, widely adopted goal-based engine. Investor.gov is the free research and calculator baseline that complements any paid platform.

The practical move is to match the tool to your dominant workflow rather than the longest feature list. If most of your value is deep planning and aggregation, start with eMoney. If it's client collaboration and clean presentation, start with RightCapital. If transparency and predictable cost matter most, start with Moneytree. Run a trial where one is offered, put a real client scenario through it, and watch how fast the software handles the "what if" question that always comes up in the meeting. The platform that answers it cleanly, in front of the client, is the one that earns its place in your stack.

FAQs

Financial advisor software is used to model client scenarios, build financial plans, present those plans clearly, and collaborate with clients between meetings. It covers retirement planning, tax planning, cash flow planning, and scenario modeling, and typically includes a client portal for ongoing collaboration. For a firm, it also standardizes how advisors build and deliver plans so the workflow scales.

RightCapital and eMoney Advisor are both strong on client collaboration. RightCapital pairs a client-friendly advisor client portal with visual outputs like Snapshot and Blueprint, while eMoney combines account aggregation with a client portal and mobile app. The best choice depends on whether you prioritize visual simplicity or aggregated financial depth in the client experience.

RightCapital, eMoney Advisor, and Envestnet | MoneyGuide all offer robust retirement planning software with Monte Carlo analysis. RightCapital presents retirement scenarios in a clean, client-readable format, eMoney adds account aggregation for accuracy, and MoneyGuide brings a mature goal-based engine. All three handle serious retirement projections; the differentiator is how each presents results to clients.

Investor.gov is the closest to free, offering SEC-backed calculators, retirement tools, and research at no cost. It is not a full planning platform and will not build or store client plans, but it is a credible free supplement for calculators and education. Commercial financial planning software for advisors generally requires a paid subscription.

Prioritize planning depth (retirement, tax, and scenario modeling), client portal and collaboration quality, plan presentation, and workflow repeatability across your team. Integration with your existing CRM and custodian matters too, since fragmented data creates manual work. Weight these against how your specific clients consume plans.

A client portal moves collaboration out of scattered emails and into a shared, secure space where clients view plans, upload documents, and track progress on their own time. That keeps plans current between meetings and reduces status-check requests. For advisors, it strengthens retention because clients stay engaged with their plan rather than forgetting it until the annual review.

Financial planning software models and presents client plans, running retirement, tax, and cash flow projections. CRM software manages the relationship and pipeline: contacts, tasks, communication history, and workflows. Most RIA software stacks use both, with the planning tool feeding client-facing plans and the CRM handling operations, and the two often integrate.

Normalize every option to an annual per-seat cost, since some vendors bill per advisor monthly and others per user annually. RightCapital and Moneytree publish pricing openly, while eMoney Advisor requires a quote and MoneyGuide lists a base subscription with separate add-ons. Factor in aggregation fees, integration add-ons, and contract terms to compare true total cost across the advisor tech stack.